Top 50 P&C Coretech Ecosystem Partners: Structural Areas of Focus

Across 39 P&C core platforms, we identified more than 600 publicly announced ecosystem partners.

68% appear in only one ecosystem.

50 stand out from the crowd. These partners appear repeatedly across platforms, and signal capabilities that insurers prioritize highly.

Executive Summary

Modern P&C core platforms compete both on core functionality and the strength of their ecosystems.

P&C coretech ecosystems have expanded significantly over the last six years. In a review of 39 core platform vendors active in the United States and Canada, Coretech Insight identified over 600 publicly announced ecosystem partners that span 177 capabilities.

While most partner with only one platform, a subset of 50 partners appears repeatedly across multiple ecosystems. When mapped to capabilities, these Top 50 partners form a three-part model for evaluating ecosystem balance, maturity, and strategic positioning.

Key Insights:

Most ecosystem partners have limited adoption.

68% of publicly announced partners appear in only one ecosystem; broad cross-platform adoption is rare.The Top 50 partners signal buyer priorities.

These partners recur across ecosystems and align closely with the most consistently prioritized insurance capabilities.The ecosystem capabilities provided by these partners cluster into three areas of focus:

Foundational enterprise capabilities

Insurance operations and risk control

Acceleration through engagement, automation, and analytics.

Ecosystem structure reflects strategic focus.

Heavier investment in operations versus acceleration often correlates with target markets, LOBs, customer profiles, and platform architecture.

Explore Further:

The resources below expand on the ecosystem structure and partner patterns discussed in this article. These patterns reveal a structural model that can help vendors, buyers, and ecosystem partners better understand how modern P&C coretech ecosystems are built and evaluate their fit for purpose.

View the Top 50 ecosystem partners organized by structural area of focus

See how ecosystem partners cluster around foundational, operational, and acceleration capabilities.Download the full Top 50 partners matrix

A detailed view of the Top 50 partners mapped to ecosystem capabilities.Explore illustrative Top 50 ecosystem profiles for both new and established coretech platforms

See how different ecosystem structures reflect platform strategy, market focus, and architectural posture.Read Mapping the P&C Coretech Ecosystem: 177 Capabilities that Shape Ecosystem Coverage and Fit

A deeper look at the capability framework used to evaluate ecosystem structure and coverage.

Analysis

The number of P&C coretech ecosystem partner announcements has surged over the last six years. In our Q4 2025 review of P&C core platform ecosystems, we identified over 600 partners featured in press releases and online partner and marketplace listings.

Nearly 70% of partners participate in only one ecosystem

Most partners – 68% – appear in only one ecosystem. This is not a surprise. Ecosystems often serve as a tech incubator, giving coretech vendors and their customers access to emerging technologies/solutions, while providing ecosystem partners with access to new markets. Many ecosystem partners are start-ups and early-stage insurtechs proving the commercial viability of their offerings.

At the other end of the spectrum, we identified a group of 50 partners that appear in multiple ecosystems. When we mapped them to our ecosystem capabilities framework, a three-part pattern emerged.

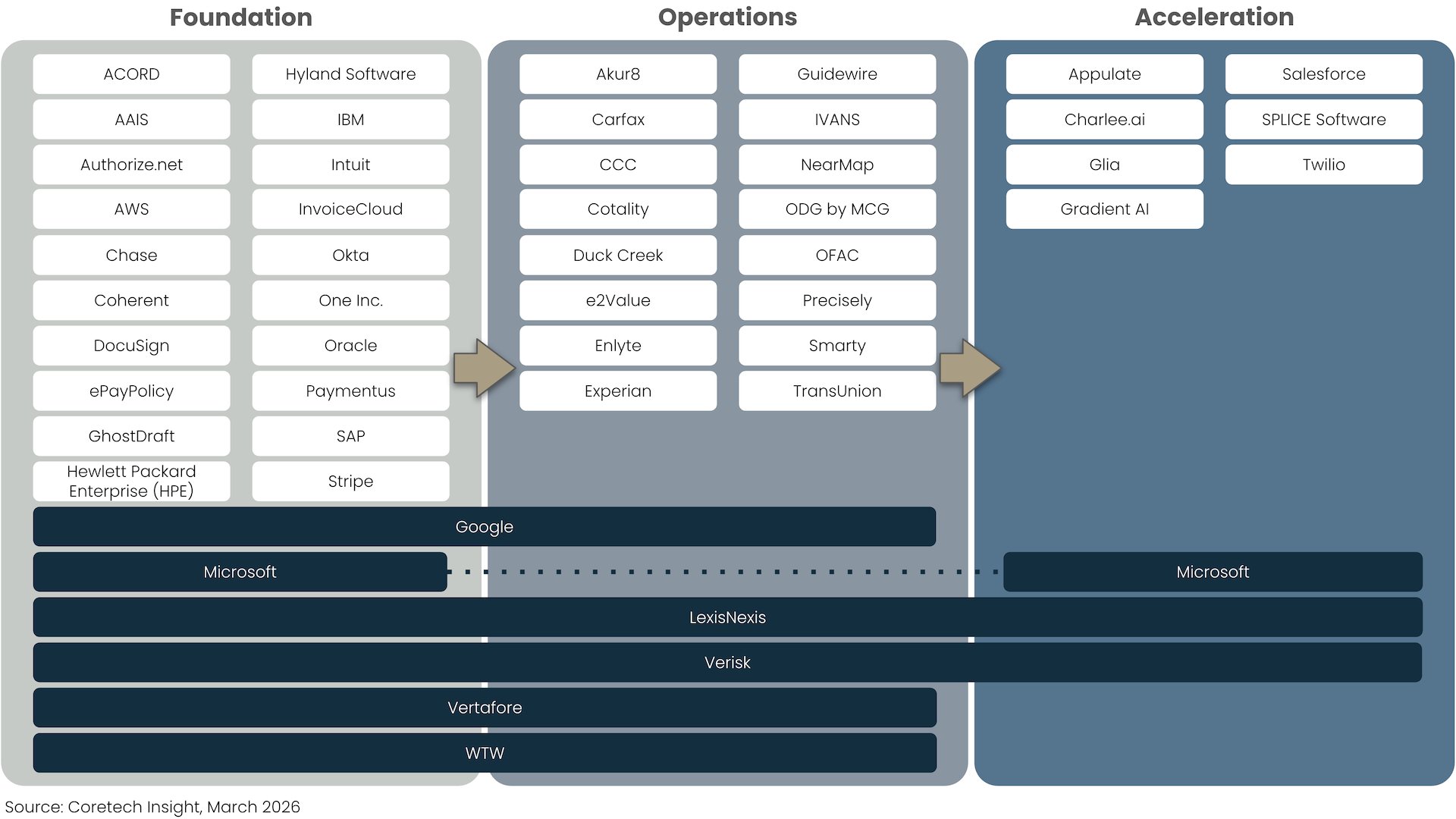

Foundation, Operations, and Acceleration

Figure 1, below, shows how these partners appear in the following three structural areas of focus, based on the roles they play in the P&C insurance industry:

Foundational enterprise capabilities

Insurance operations

Acceleration through engagement, automation, and analytics

Figure 1. Top 50 P&C Coretech Ecosystem Partners by Structural Area of Focus

From Foundational Infrastructure to Acceleration

The first area of focus includes partners that are foundational for conducting P&C insurance operations at enterprise scale – standards, industry data, financial transactions, document management, IT/cloud infrastructure, and back-office alignment. (See Table 1.)

Table 1. Foundation: Enterprise Capabilities and Core Financial Readiness

| FOUNDATION | |||||||

|---|---|---|---|---|---|---|---|

| Enterprise infrastructure and platform readiness | |||||||

| Category | Capability | Total Partners● | Top 50 Partner(s) | Role | |||

| 01. | Industry Standards, Classification, and● Actuarial Products & Services | 01.02. | Standards & Classification Systems | 6 | AAIS, ACORD | Standards alignment for insurance classification | |

| 08. | Data Providers (Cross-Domain, Other) | 08.07. | Insurance Industry Data (Cross-Domain)● | 6 | LexisNexis, Verisk, WTW | Industry data validation for underwriting● and compliance | |

| 13. | Payments, Billing, Premium Finance & Financial Services | 13.03. | Payments | 46 | Authorize.net, Chase, Duck Creek, ePayPolicy, InvoiceCloud, One Inc.,● Paymentus, Stripe | Payment processing infrastructure for premium and claims flows | |

| 16. | Enterprise Content Management & E-Signature | 16.01. 16.02. | Document / Data Ingestion Intelligent Document Processing | 14 | Coherent, GhostDraft, Hyland Software, Vertafore | Enterprise document governance and records management | |

| 16.05. | E-signature | 9 | DocuSign, Dropbox | Digital transaction completion | |||

| 26. | IT Infrastructure, DevOps, Security & Platforms | 26.03. | IT Infrastructure, Solutions, and Services | 5 | Hewlett Packard Enterprise (HPE),● IBM | Enterprise infrastructure for traditional and hybrid deployments | |

| 26.04. 26.05. | Cloud Infrastructure, Solutions, and Services● Identity Management | 12 | AWS, Google, Microsoft, Okta, Oracle, SAP | Scalable cloud infrastructure with secure● identity management | |||

| 29. | Financial, ERP, and Back-Office Systems● | 29.01. 29.02. | Enterprise Resource Planning (ERP) Financial & Accounting Technology Solutions | 15 | Intuit, Microsoft, Oracle | Financial system integration for accounting and reporting | |

| Source: Coretech Insight, March 2026 | |||||||

The second area of focus covers capabilities important for operational domains, such as specific LOBs and risk markets. (See Table 2.) Within this area, we begin to see clearer differences among ecosystems. For example, a heavier focus on personal lines, commercial lines, or workers’ comp will drive a different partner mix.

Table 2. Operations: Insurance Domain Operations & Risk Control

| OPERATIONS | |||||||

|---|---|---|---|---|---|---|---|

| Insurance workflows and risk intelligence | |||||||

| Category | Capability | Total Partners● | Top 50 Partner(s) | Role | |||

| 03. | Insurance Product Development | 03.01. | Product Models | 10 | Verisk | Insurance product modeling and configuration | |

| 04. | Agency/Broker Management & Distribution | 04.01. 04.04. 04.06. | Agency Management Systems Connectivity & Data Exchange Distribution Management | 14 | IVANS, Vertafore | Distribution channel enablement | |

| 04.09 | Licensing & Appointment Compliance | 3 | Vertafore | Producer licensing and appointment compliance | |||

| 05. | Property Data, Geospatial Intelligence & Hazard Analytics | 05.01. 05.06. | Address Data Intelligence Mapping | 11 | Google, Precisely, Smarty, Verisk | Geospatial validation and address normalization | |

| 05.02. | Property/Location Data & Insights | 32 | Cotality, Guidewire, LexisNexis, Nearmap, Verisk | Property risk assessment & underwriting validation | |||

| 05.05. | Building Insights & Replacement Cost Estimates | 2 | e2Value, Verisk | Replacement cost estimation and property valuation | |||

| 06. | Vehicle Data, Telematics & Vehicle Intelligence | 06.01. | Data & Insights - Vehicle / VIN | 14 | Carfax, LexisNexis, Verisk | Vehicle risk validation and underwriting enrichment | |

| 08. | Data Providers (Cross-Domain, Other) | 08.01. | Commercial & Business Data | 15 | Experian, Verisk | Commercial risk profiling and underwriting enrichment | |

| 08.02. | Consumer & Demographic Data | 7 | Experian, LexisNexis, TransUnion,● Verisk | Consumer risk scoring and underwriting segmentation | |||

| 08.04. | Public Records & Government Data | 7 | LexisNexis | Public record verification and compliance support | |||

| 08.08. | Insurance Loss History | 2 | LexisNexis, Verisk | Prior loss validation and underwriting risk evaluation | |||

| 08.09. | Insurance Coverage Verification | 1 | Verisk | Coverage verification and claims validation support | |||

| 10. | Fraud, Identity Verification & Compliance● | 10.01. 10.03. | AML / sanctions screening Fraud Detection & Analytics | 22 | LexisNexis, OFAC, Verisk | Fraud prevention, identity verification, and regulatory compliance | |

| 12. | Policy Rating & Quoting | 12.01. | Pricing / Rating | 7 | Akur8, WTW | Pricing optimization and rating support● | |

| 13. | Payments, Billing, Premium Finance & Financial Services | 13.04 | Premium Finance | 7 | Vertafore | Premium financing enablement and funds flow flexibility | |

| 15. | Insurance Software Solutions & Services (Cross-Domain, Non-Core) | 15.01 | Insurance Software Solutions and Services | 3 | Vertafore | Specialized insurance workflow extensions | |

| 19. | Policy Servicing & Notifications | 19.02 | Policy Servicing | 2 | LexisNexis | Policy servicing workflow integration | |

| 20. | Claims Management & Loss Adjustment | 20.08. 20.14. | Claim Valuation & Servicing TPA / Claim Service Solutions | 20 | CCC, Enlyte | Core claims workflow depth | |

| 20.13. | Subrogation Services | 6 | CCC | Claims recovery and subrogation management support | |||

| 21. | Inspections | 21.02. | Inspection Field Solutions | 5 | Duck Creek | Field inspection and risk assessment enablement | |

| 22. | Workers' Compensation Solutions and Services | 22.03. 22.06. 22.09. | Medical Bill Review, Provider Networks, PBM Solutions Medical Treatment / Return to Work Workers' Comp Compliance & Reporting● | 16 | ODG by MCG, Verisk | Workers’ comp medical and compliance specialization | |

| 30. | Regulatory Compliance Management & Reporting | 30.02. 30.03. | Insurer Statistical & Regulatory Reporting Regulatory Compliance Management | 8 | LexisNexis, Verisk | Regulatory reporting and statutory compliance | |

| Source: Coretech Insight, March 2026 | |||||||

Table 3 shows the third area of focus, Acceleration, which is composed of partners that strengthen customer engagement, automation, and analytics. These capabilities are important – in fact, increasingly essential – but not as foundational or embedded in insurance workflows as the first two areas. Adoption of these capabilities lags in more conservative market segments with an emphasis on traditional business processes. Higher adoption can signal a more tech-forward ecosystem correlated with:

MGAs

Digital-first carriers

Growth-stage platforms

API-centric architectures

Table 3. Acceleration: Engagement, Automation, and Analytics

| ACCELERATION | |||||||

|---|---|---|---|---|---|---|---|

| Engagement, automation, and analytics | |||||||

| Category | Capability | Total Partners● | Top 50 Partner(s) | Role | |||

| 04. | Agency/Broker Management & Distribution | 04.07. | Submissions Intake & Intake Automation● | 8 | Appulate | Submission intake automation and workflow acceleration | |

| 05. | Property Data, Geospatial Intelligence & Hazard Analytics | 05.04. | Address-specific Weather Impact Analysis | 2 | Verisk | Weather risk enrichment and exposure● analytics | |

| 17. | Customer Engagement, Communications, & Service Tools | 17.04. | CRM | 5 | Salesforce | Customer relationship orchestration | |

| 17.05. 17.06. | Customer communications management● Customer Engagement | 25 | Glia, SPLICE Software, Twilio | Digital communications and customer● engagement enablement | |||

| 20. | Claims Management & Loss Adjustment● | 20.01. | Claim Ingestion | 9 | LexisNexis | Digital first notice of loss (FNOL) and intake automation | |

| 25. | BI, Data Tools, & Analytics | 25.01. 25.02. 25.04. | BI & Analytics Predictive Analytics Reports & Report Enhancements | 17 | Charlee.ai, Gradient AI, Microsoft,● Verisk | Operational analytics, reporting, and predictive decision support | |

| Source: Coretech Insight, March 2026 | |||||||

Most Top 50 partners have a narrow focus

As these three areas of focus illustrate, most Top 50 partners are known within P&C coretech ecosystems for their focus on a specific capability, such as payments, e-signature, or document processing. Their high visibility in specific capabilities reflects the strength of their offerings and their successful track record.

A small subset of partners – Google, Microsoft, LexisNexis, Verisk, Vertafore, and WTW – have a wider range of solutions spanning multiple layers and capabilities. Google and Microsoft are industry-agnostic cloud infrastructure providers that also have other solutions widely adopted in P&C coretech – for address/mapping, in the case of Google, and for ERP and BI and analytics for Microsoft. In contrast, Vertafore and WTW are focused on the insurance industry, and offer a range of insurance data and product solutions.

Duck Creek and Guidewire are unique because they each have built prominent P&C core platforms with large ecosystems, and have also secured their places on this list through acquisitions of other solutions that appear in multiple coretech ecosystems.

LexisNexis and Verisk are in a league of their own. Out of the 39 ecosystems we reviewed, over two dozen have announced Verisk as a partner for various solutions, and 19 have announced LexisNexis as a partner. Both companies offer data and insurance solutions that span all three areas of focus and multiple categories. Their range of offerings is so broad it makes classifying ecosystem capabilities difficult. Less mature ecosystems often publicize only a vendor name or logo. A single logo can represent a partner known for a single capability, but it fails to convey the potentially dozens of capabilities that LexisNexis and Verisk might support within an ecosystem.

It’s important to note that LexisNexis and Verisk are not the only vendors that offer solutions covering multiple capabilities. Many other vendors also do so; however, the level of adoption and visibility for these other solutions within P&C coretech ecosystems is much lower. In this review, we’ve focused on the primary solutions that appear in multiple ecosystems, and we have excluded a number of other, secondary solutions offered by these partners that appear in only one ecosystem.

Application

In our last research article, we introduced a P&C coretech ecosystem capability framework. There is a strong overlap between the Top 50 ecosystem partners and the Top 10 ecosystem capabilities from the framework, with these top partners covering all top 10 and most outlier capabilities strong in specific ecosystem types.

When we apply this three-part model across ecosystems, clear patterns begin to emerge. Some ecosystems are heavily concentrated in the second area of focus, Operations. Others show relatively greater investment in the third area of focus, Acceleration. These differences often align with target markets, customer profiles, and product strategies.

This model can provide an important benchmarking and planning reference for coretech providers. The two scenarios below show how coretech vendors at different stages and with different profiles can apply this model to improve their ecosystems.

Scenario 1: Building an “MVP” Ecosystem

Imagine you’re a coretech vendor entering the US and Canada for the first time, either as a startup or from another region. You have a full platform – policy, billing, and claims + digital experience and data – and you’re targeting standard personal and commercial lines, such as auto, home, farm, and small/mainstreet commercial lines. Your platform is modern, low/no-code, cloud & AI-native, and built on .NET Core. It checks all the tech buzzword boxes. Without ecosystem partners, though, you’re dead in the water. Where should you begin to establish an initial, credible set of partners?

For your profile and current targets, some capabilities are critical, others are unnecessary. (See Table 4.)

Table 4. Scenario 1: Ecosystem Capabilities Assessment

| Essential Capabilities | Non-essential Capabilities |

|---|---|

| ●●● Property data | ●●● WC medical networks |

| ●●● VIN & vehicle data | ●●● Heavy commercial risk scoring |

| ●●● ISO / rating data alignmentXXX | ●●● Fleet telematics |

| ●●● Agency connectivity | ●●● Specialty inspection vendors |

| ●●● Claims valuation | ●●● Complex reinsurance ecosystemsXXX |

| ●●● Payments | |

| Source: Coretech Insight, March 2026 | |

Table 5 shows how applying this view of essential and non-essential capabilities to the Top 50 yields the following potential partners:

Table 5. Scenario 1: MVP Capabilities and Ecosystem Partners

| Foundation | Operations | Acceleration | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Capability | Partner | Capability | Partner | Capability | Partner | |||||

| 08.07. | Insurance Industry Data (Cross-Domain) | Verisk | 04.04. | Connectivity & Data Exchange | IVANS | 17.04. | CRM (optional) | Salesforce | ||

| 13.03. | Payments | One Inc. | 05.01. | Address Data Intelligence | Smarty | 17.05. | Customer communications management | Twilio | ||

| 16.01. 16.02. | Document / Data Ingestion Intelligent Document Processing | GhostDraft● | 05.02. 05.05. | Property/Location Data & Insights Building Insights & Replacement Cost● Estimates | Verisk | 25.01. | BI & Analytics | Microsoft | ||

| 16.05. | E-signature | Docusign | 06.01. | Data & Insights - Vehicle / VIN | Verisk | 25.02. | Predictive Analytics (optional)● | Gradient AIXX | ||

| 26.04. | Cloud Infrastructure, Solutions, and● Services | Microsoft | 08.08. | Insurance Loss History | LexisNexisXX | |||||

| 10.03. | Fraud Detection & Analytics | LexisNexis | ||||||||

| 20.08. | Claim Valuation & Servicing | CCC | ||||||||

| Source: Coretech Insight, March 2026 | ||||||||||

With this approach, a base ecosystem could be the following 10 partners:

CCC

DocuSign

GhostDraft

IVANS

LexisNexis

Microsoft

One Inc.

Smarty

Twilio

Verisk

These initial partners provide the coretech platform with a credible start at supporting agent-based distribution, quote/bind/issue, fraud mitigation, payments, and claims intake & processing.

Scenario 2: Refreshing an Established P&C Coretech Platform

Imagine that, instead of a new market entrant, you’re a well-established coretech provider in the market for well over a decade. (Note: this scenario is based on an anonymized, real-world P&C coretech platform.) You also have a relatively modern core platform targeting standard personal and commercial lines. Over the years, through your dealings with various customers, you’ve accumulated a collection of several dozen partners that are listed on your website, including three dozen that align with the top 50 vendors and associated categories.

How does your partner ecosystem stack up? Are there gaps or new opportunities you should address?

Table 6, below, shows your current complement of ecosystem partners for your foundation.

Table 6. Scenario 2: Foundational Ecosystem Partners and Capabilities

| Foundation | ||

|---|---|---|

| Capability | Ecosystem Partner(s) | |

| 01.02. | Standards & Classification Systems | AAIS, Mutual Service Office (MSO) |

| 08.07. | Insurance Industry Data (Cross-Domain) | LexisNexis |

| 13.03. | Payments | Authorize.net, eZpay, One Inc., Western Union● |

| 16.01. 16.02. | Document / Data Ingestion Intelligent Document Processing | DocFinity, Hyland Software, Vertafore |

| 16.05. | E-signature | DocuSign, eSign |

| 26.03. | IT Infrastructure, Solutions, and Services | |

| 26.04. 26.05. | Cloud Infrastructure, Solutions, and Services Identity Management | Microsoft, Oracle, SAP |

| 29.01. 29.02. | Enterprise Resource Planning (ERP) Financial & Accounting Technology Solutions● | Fiserv, Microsoft, Oracle, Sage |

| Source: Coretech Insight, March 2026 | ||

In your foundation, every capability is covered except for IT infrastructure. This capability is oriented toward on-prem implementations, and all your customers are deployed via the cloud. You conclude overall coverage for this area is sufficient.

Table 7 shows your current complement of partners for operations.

Table 7. Scenario 2: Ecosystem Partners and Capabilities for Operations

| Operations | ||

|---|---|---|

| Capability | Ecosystem Partner(s) | |

| 03.01. | Product Models | |

| 04.01. 04.04. 04.06. | Agency Management Systems Connectivity & Data Exchange Distribution Management | Applied Systems, IVANS, Vertafore |

| 04.09 | Licensing & Appointment Compliance | |

| 05.01. 05.06. | Address Data Intelligence Mapping | Verisk |

| 05.02. | Property/Location Data & Insights | Cotality, EagleView, Verisk |

| 05.05. | Building Insights & Replacement Cost Estimates | e2Value, Verisk |

| 06.01. | Data & Insights - Vehicle / VIN | Carfax, Highway Loss Data Institute (HLDI),S&P Global, Verisk● |

| 08.01. | Commercial & Business Data | Verisk |

| 08.02. | Consumer & Demographic Data | Equifax, LexisNexis, TransUnion |

| 08.04. | Public Records & Government Data | |

| 08.08. | Insurance Loss History | Verisk |

| 08.09. | Insurance Coverage Verification | Verisk |

| 10.01. 10.03. | AML / sanctions screening Fraud Detection & Analytics | OFAC, Verisk |

| 12.01. | Pricing / Rating | |

| 13.04 | Premium Finance | |

| 15.01 | Insurance Software Solutions and Services | Ebix, Vertafore |

| 19.02 | Policy Servicing | |

| 20.08. 20.14. | Claim Valuation & Servicing TPA / Claim Service Solutions | CCC, Corvel, Enlyte, Solera Lynx |

| 20.13. | Subrogation Services | |

| 21.02. | Inspection Field Solutions | JMI Reports |

| 22.03. 22.06. 22.09. | Medical Bill Review, Provider Networks, PBM Solutions● Medical Treatment / Return to Work Workers' Comp Compliance & Reporting | ExamWorks |

| 30.02. 30.03. | Insurer Statistical & Regulatory Reporting Regulatory Compliance Management | |

| Source: Coretech Insight, March 2026 | ||

There are a few gaps (highlighted in blue). Some apparent gaps, such as product models, pricing/rating, and policy servicing, are actually already fully addressed within your core platform, so ecosystem partners are not necessary for these. There may be opportunities to fill other potential gaps, though, such as licensing and appointment compliance, public and government data, subrogation, and regulatory compliance management and reporting. You may also have existing relationships that need to be formalized and publicized, to avoid the appearance of gaps that do not really exist. You recognized these opportunities for improvement, but you conclude that coverage for Operations is also good overall.

Table 8 shows your current complement of partners for the third area, Acceleration.

Table 8. Scenario 2: Ecosystem Partners and Capabilities for Acceleration

| Acceleration | ||

|---|---|---|

| Capability | Ecosystem Partner(s)● | |

| 04.07. | Submissions Intake & Intake Automation | Appulate |

| 05.04. | Address-specific Weather Impact Analysis● | |

| 17.04. | CRM | |

| 17.05. 17.06. | Customer communications management Customer Engagement | |

| 20.01. | Claim Ingestion | |

| 25.01. 25.02. 25.04. | BI & Analytics Predictive Analytics Reports & Report Enhancements | |

| Source: Coretech Insight, March 2026 | ||

Here you see more opportunity for improvement. Your platform is known for being comprehensive and reliable for your supported LOBs, but it is not known for innovative digital capabilities or advanced analytics. These gaps reveal where the strategic addition of a few partners may help round out already operationally strong capabilities and expand your market reach. From the top 50 list, you establish a short list of candidates for further investigation:

Weather impact analysis - Verisk

CRM - Salesforce

CCM - Twilio

Claim Ingestion – LexisNexis

BI & Analytics - Microsoft

Predictive Analytics - Gradient AI

Three of these vendors – LexisNexis, Microsoft, and Verisk – are already partners, which may enable faster adoption of these solutions. As with the operational gaps, there may be an opportunity to formalize and/or publicize existing relationships to bolster your public coverage of these customer engagement, automation, and analytics capabilities.

Also, it’s important to note that treating these as gaps assumes these capabilities are important to this coretech provider. It could easily and legitimately be the case that these are not priorities for this vendor. Instead of showing gaps, the light coverage may reflect this vendor’s strategic choices.

Application for buyers and ecosystem partners

These examples are not a recommendation for or endorsement of any of the ecosystem partners listed above. For nearly every capability, there are several alternative competitive options. (In some cases, there are dozens.) These examples show how selection of a small, initial set of widely adopted vendors could provide broad coverage of essential categories, and how strategic selection of a few additional partners could close existing gaps. For our first example, the list of partners is simply a starting point for a credible ecosystem that should continue to grow and evolve as the coretech vendor engages with the market.

This three-part model for the Top 50 partners also has value for coretech buyers and other ecosystem partners. For buyers, it enables them to assess a coretech vendor’s ecosystem structure at a more granular level. If you’re tech-forward and innovative, does the coretech candidate’s ecosystem reflect this? Or, like in the example above, is it oriented toward traditional operations and light on innovation and engagement?

For ecosystem partners, especially those that directly compete with the Top 50, this model can help pinpoint opportunities. In large ecosystems, it is common for two or more partners to cover the same capability. This allows for more choices and a wider range of functionality. If your Top 50 competitor is already embedded in an ecosystem, they’ve confirmed there is a need – you may have an opportunity to engage to provide an alternative. If they haven’t yet partnered with an ecosystem – especially a growing ecosystem – you may have an opportunity to step in first to meet that need.

The ecosystem is the platform

For a modern P&C core platform, the surrounding ecosystem increasingly defines its boundaries.

In other words, the ecosystem is the platform.

For all stakeholders – vendors, buyers, and partners – the structure of a coretech ecosystem offers a powerful signal of platform strategy and market fit. Understanding a provider’s relationships with the Top 50 partners and their associated capabilities provides a practical way to evaluate platform maturity, market focus, and long-term viability.

Recommendations

Coretech Vendors:

Tend to your foundation before you expand. Don’t chase emerging/differentiating capabilities at the expense of strong foundational and operational capabilities.

Ensure your operational capabilities are coherent. Before adding additional partners, assess your operational capabilities to identify where coverage lacks depth, and where adjacent capabilities might be added or better aligned to provide more value.

Use partner selection to signal positioning. Mainstream partners signal credibility. Specialists signal depth. Emerging vendors signal innovation. Be deliberate about what your ecosystem signals to buyers.

Coretech Buyers:

Identify the critical capabilities (and, ideally, partners) for your organization’s areas of focus. Use these to create an ideal ecosystem map to help assess coretech platform and ecosystem fit.

Focus on ecosystem coverage of critical capabilities. Don’t get distracted counting partner logos; confirm ecosystem partners cover your essential capabilities across all levels.

Verify unpublished partnership claims. Some coretech vendors will insist they have an unpublished relationship with a partner; these claims should be investigated and confirmed. It is the mark of a mature vendor to have a current, sufficiently detailed and public list of its partners and their solutions.

Ecosystem Partners:

Use the Top 50 vendors and capabilities to profile ecosystems. Target ecosystems that share a common focus and offer opportunities for differentiation; limit your investment in ecosystems that signal misalignment.

Avoid entering overcrowded capabilities without differentiation. In high-density domains with many potential partners – such as payments or property data – differentiation must be clear.

Align your solutions and value propositions with insurance operations. Operational workflows offer more durable partnership opportunities than generic innovation categories.

For organizations seeking to apply this research — including detailed ecosystem benchmarks, vendor-specific insights and comparisons, and strategic fit assessments — Coretech Insight provides private research reports and executive briefings tailored to buyers, vendors, and ecosystem partners.

To explore a private briefing or customized research engagement, contact Coretech Insight at jeff.haner@coretechinsight.com.

Note 1. Methodology

This article builds on ecosystem research conducted by Coretech Insight in Q4 2025. The research analyzed publicly available ecosystem, partner, and marketplace content for 39 P&C coretech vendors actively marketing in the United States and Canada.

We reviewed ecosystem presentations, partner directories, marketplace listings, and more than 450 press releases announcing technology partnerships over the past 15 years. From this analysis, we catalogued 647 ecosystem partners and developed a structured capability framework comprising 30 first-level categories and 177 second-level capabilities.

Each capability was assessed for coverage based on the presence of at least one publicly announced partner within that capability area. This research is designed to identify structural ecosystem patterns and strategic emphasis — not to audit integration depth, contractual status, production usage, or commercial success.

Important caveats:

This analysis focuses on technology and solution partners. Ecosystem partners were included when they provide integrated technology solutions, applications, or platform extensions typically reflected in partner directories or marketplaces. Professional services firms, system integrators, and implementation partners were not included, as this research evaluates ecosystem capability coverage rather than delivery capacity.

Partnership inclusion reflects vendor-acknowledged relationships. This analysis includes ecosystem partners publicly identified by coretech vendors in press releases, partner directories, or marketplace listings. Some technology providers may independently claim partnerships that are not formally announced by the coretech vendor. Such claims were not included in order to maintain consistent inclusion criteria across vendors.

Public information may be incomplete. Some vendors maintain integration libraries or partner relationships that are not fully disclosed in public materials.

Coverage indicates presence, not quality. A capability is considered “covered” if at least one partner exists in that area. This does not measure integration depth, deployment frequency, revenue contribution, or the maturity of the relationship.

Gaps may be intentional. Missing capabilities often reflect strategic positioning rather than technical limitations. Vendors prioritize ecosystem investment based on target markets, product strategy, and operating model.

This research represents a point-in-time analysis. Ecosystems evolve continuously, with new partnerships announced regularly. While Coretech Insight intends to update and refine this dataset periodically, this analysis reflects publicly available information as of Q4 2025.

Despite these limitations, publicly shared ecosystem content provides a meaningful signal of vendor strategy, partner prioritization, investment in extensibility, and the role ecosystems play in go-to-market execution. This approach enables consistent cross-vendor comparison using a common structural lens.

Jeff Haner is the co-founder of Coretech Insight, an independent advisory firm. He has served in senior IT, advisory, and marketing roles with Deloitte, Oliver Wyman, NJM Insurance Group, Gartner, and BriteCore. While with Gartner, he authored the Magic Quadrant for P&C Core Platforms. Jeff’s experience “on both sides” of the insurance technology table and his ongoing research enable him to offer deep insurance industry knowledge, strategic insights, and hands-on help to take action.

Contact Jeff at jeff.haner@coretechinsight.com