Mapping the P&C Coretech Ecosystem: 177 Capabilities that Shape Ecosystem Coverage and Fit

Ecosystem capabilities are far narrower than partner counts suggest.

We analyzed 39 P&C coretech vendors and 647 publicly announced partners to map 30 ecosystem categories and 177 distinct capabilities.

Average capability coverage: 13%

This article introduces the P&C Coretech Ecosystem Capability Framework and explores how to apply this to gauge coretech vendor maturity, positioning, and strategic fit.

Executive Summary

We analyzed 39 P&C coretech vendors and 647 publicly announced partners to map the structure of today’s coretech ecosystems. The result is a framework of 30 categories and 177 distinct capabilities.

Key Insights:

Average ecosystem coverage is 13%.

Claims of expansive partner networks are common; most ecosystems cover a subset of capabilities.

Top 10 Ecosystem Capabilities reveal areas of concentration.

These capabilities cluster around data enrichment, underwriting support, digital engagement, analytics, and automation — reflecting where industry interest and buyer demand are strong.

Ecosystem composition is more important than size.

Two vendors with similar partner counts can offer materially different capabilities.

This Ecosystem Capability Framework is intended to be a shared reference for evaluating ecosystem coverage, identifying gaps, and assessing fit across the P&C coretech market.

Explore Further:

Download the full P&C Coretech Ecosystem Capability Framework – 30 categories, 177 capabilities for benchmarking and comparisons.

Review the Top 10 ecosystem capabilities to understand where coverage and buyer interest are most concentrated.

See an illustrative Vendor A / Vendor B example of how to use ecosystem shape to evaluate coretech vendor fit.

Read Ecosystems as Strategic Signal: Five Types of Coretech Ecosystems for a detailed overview of ecosystem types.

Analysis

Coretech ecosystems are promoted as expansive networks, “with hundreds of partners,” that benefit customers by giving ready access to new tech and advanced capabilities. However, it’s not easy for a customer to assess the real capabilities and business value an ecosystem might provide, or to compare ecosystems.

In Q4 2025, Coretech Insight reviewed published ecosystem press releases, partner profiles, and ecosystem/marketplace listings of 39 vendors actively marketing their P&C core platforms in the US and Canada. This review focused specifically on technology and solution partners that extend platform capabilities, rather than implementation or professional services relationships. We identified and catalogued 647 ecosystem partners with their solutions, and identified five types of P&C coretech ecosystems (see Ecosystems as Strategic Signal: Five Types of Coretech Ecosystems).

This article builds on this research and presents an ecosystem capability framework with 177 capabilities, grouped into 30 categories. We intend this capability framework to serve as a shared reference point for evaluating coretech ecosystems.

Average Coverage: 13%

Applying this framework, the average coverage of these capabilities within coretech ecosystems was 13%.

This finding is an important reality check. Robust ecosystems take time and effort to build. The P&C insurance industry is vast and fragmented, with many separate markets and market niches with unique requirements. No vendor can be all things to all comers in the industry.

The purpose of this framework is not to challenge vendor claims, but to understand the shape of ecosystem coverage. This framework helps reveal the maturity of an ecosystem, composition of its capabilities, and the decisions the coretech vendor has made about its strategic focus – shifting evaluation of ecosystems from size to alignment with buyer needs.

Buyers and other key stakeholders can use this information to more accurately gauge the fit-for-purpose of a coretech platform and its ecosystem.

30 Ecosystem Partner Categories

At the top level of the framework are 30 ecosystem partner categories (See Figure 1). These categories generally align with the insurance value chain, from product definition through policy issuance and servicing, claims, reporting, and compliance. Some categories cut across multiple stages.

Figure 1. Ecosystem Partner Categories

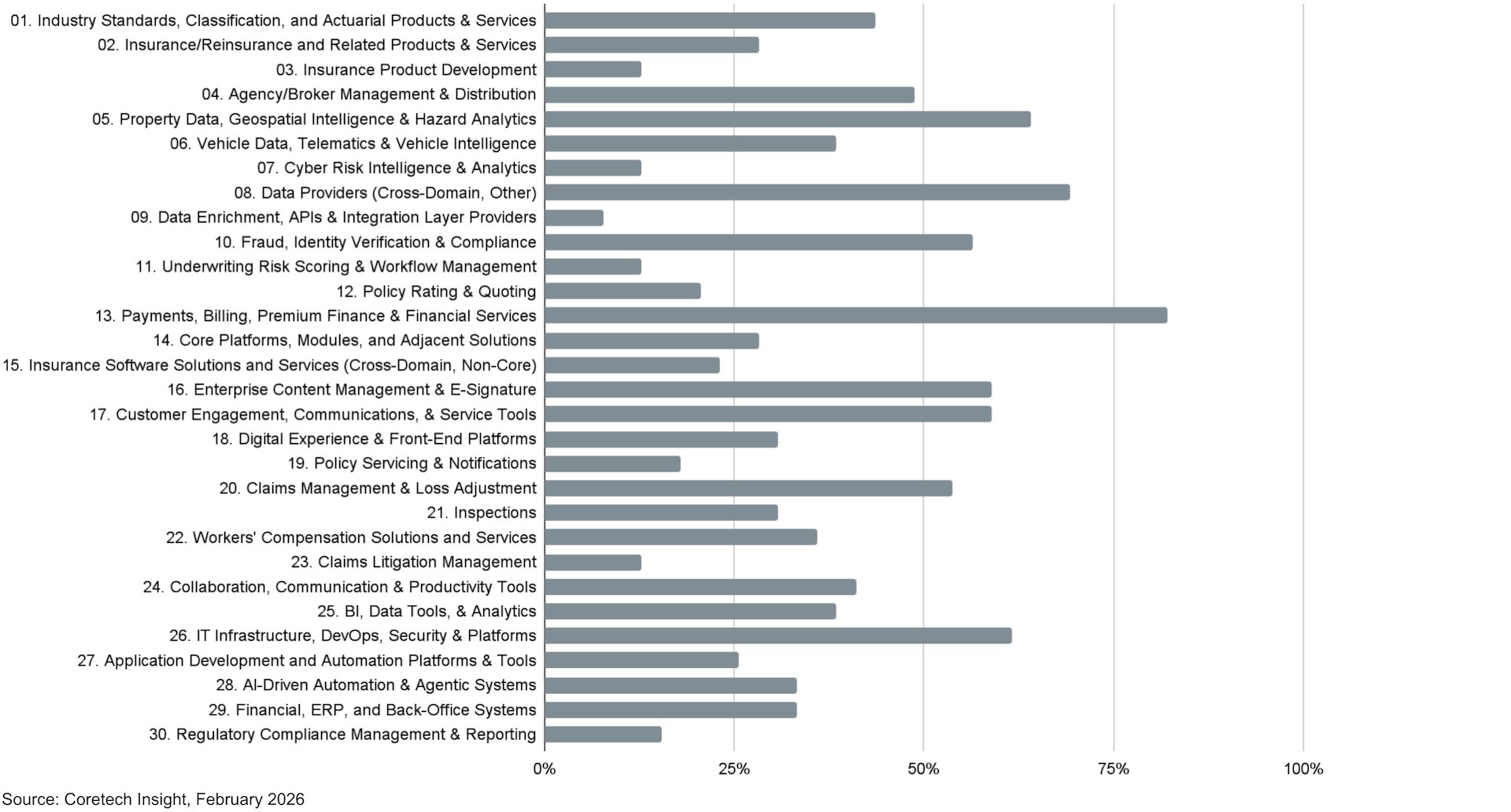

At this level, the framework enables an initial scan of an ecosystem. Figure 2 shows overall coverage for each category across the 39 vendors in our review.

Figure 2. Ecosystem Category Coverage – All Coretech Vendors

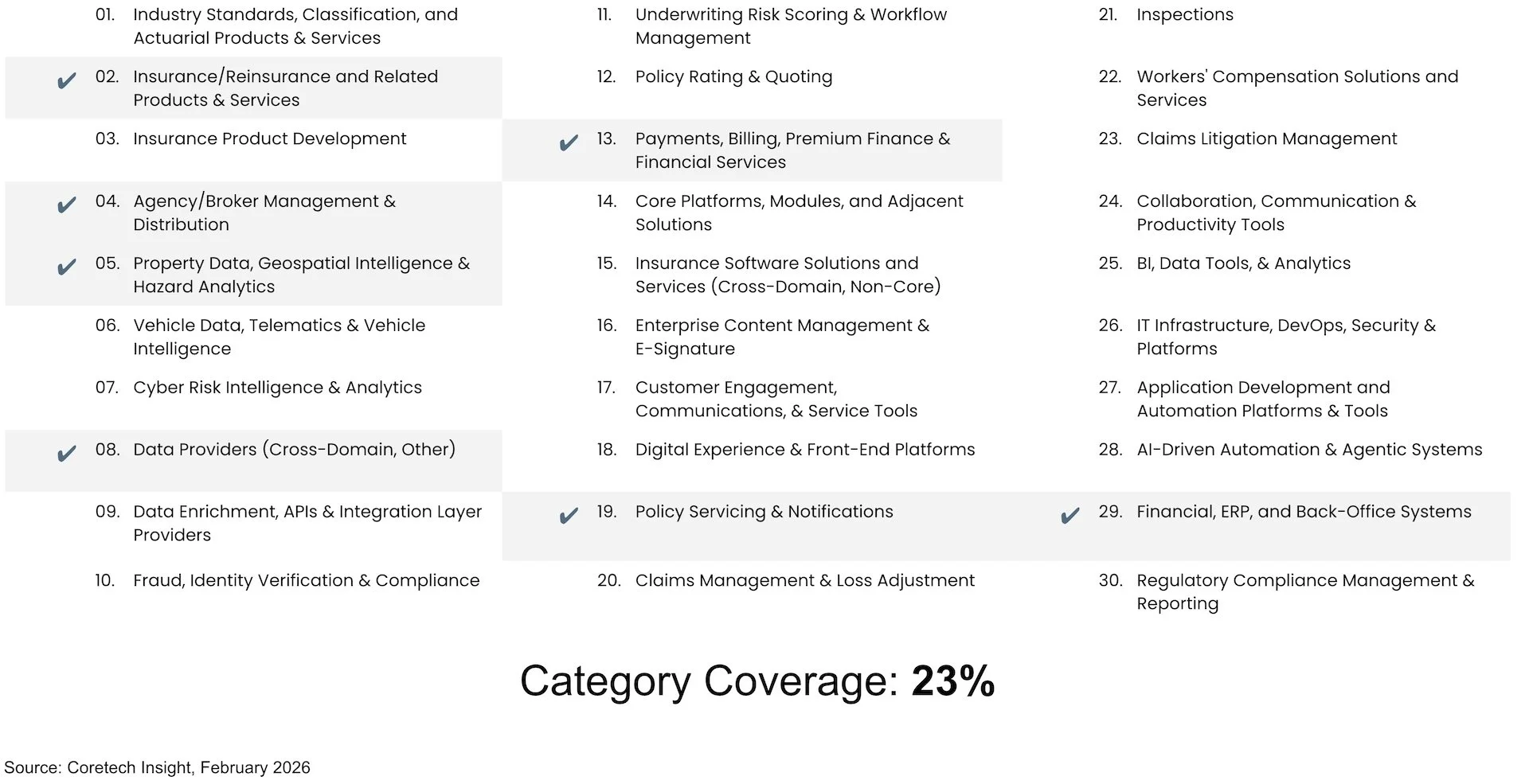

These categories help classify an ecosystem and define its shape. Figure 3 illustrates this with an example of an individual coretech vendor’s ecosystem – based on a real-world ecosystem, anonymized. This example is a product-centric ecosystem with a limited number of partners.

Figure 3. Sample Coretech Vendor Ecosystem Category Coverage

Many vendors, though, have a higher level of coverage. At least one-third of the vendors cover half or more of the categories and several cover 75% or more. While helpful for an initial scan and classification, the categories are not granular enough to clearly show differences. It’s hard to draw conclusions when nearly every category box is checked.

Moving to the next level, capabilities, provides granularity for more meaningful comparisons. Figure 4 below illustrates this.

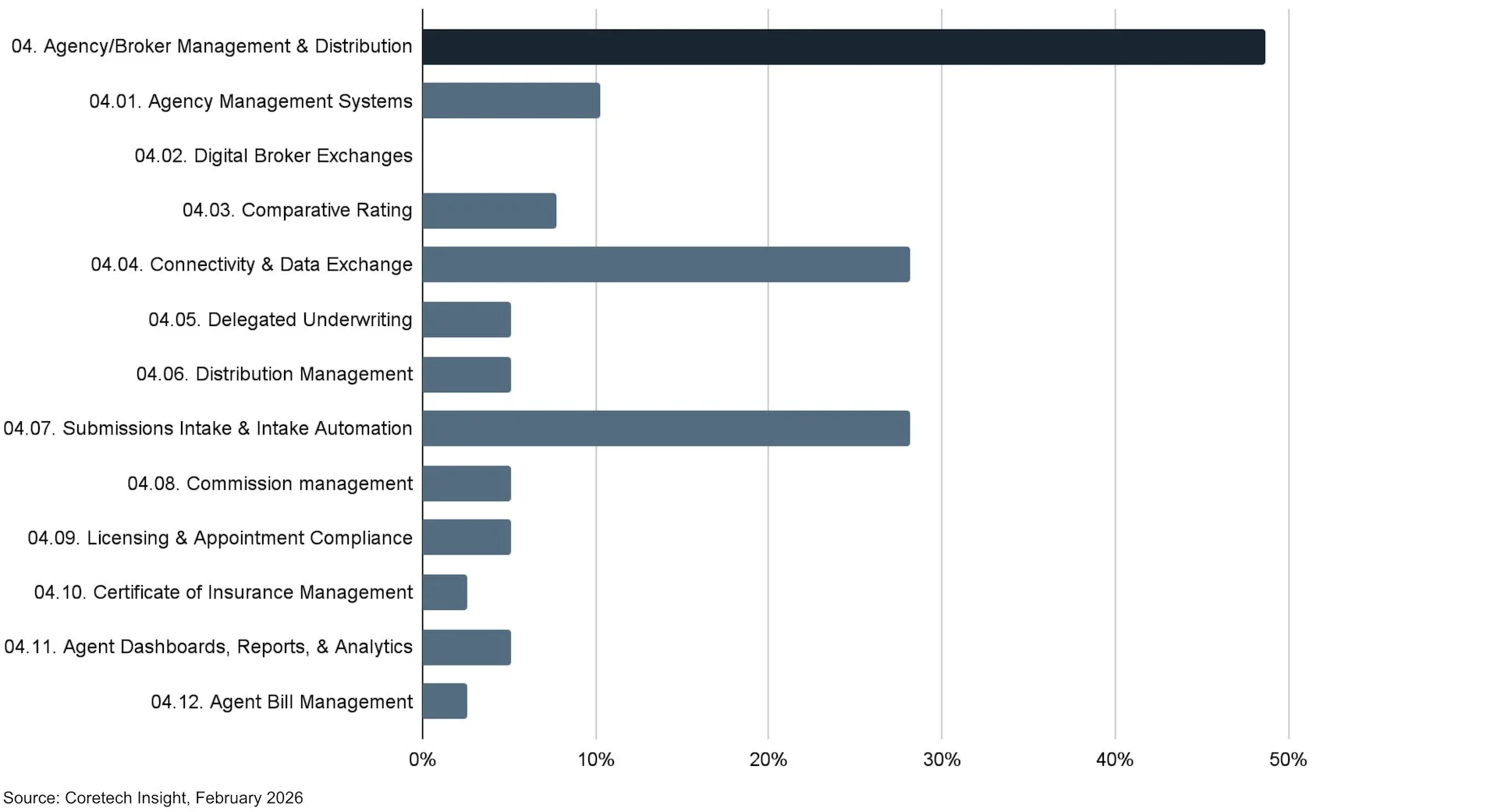

At the category level for 04. Agency/Broker Management & Distribution — the first dark navy bar in the chart — nearly half of the coretech vendors can confidently say, “Yes, we have a partner that covers agencies/brokerages and distribution.”

When we move to the second level, and assess the dozen capabilities within this category, the picture changes. Most vendor partners are concentrated in two capabilities: 04.04 Connectivity and Data Exchange and 04.07. Submission Intake & Intake Automation. Only a small percentage of vendors cover the other capabilities.

Figure 4. Category 04. Agency/Broker Management & Distribution

Note: For brevity, we have not listed all 177 ecosystem capabilities in this article. The full ecosystem framework with all categories and capabilities is available for download in PDF format at this link: Coretech Ecosystem Capability Framework.

What does coverage mean?

A capability is considered “covered” if the ecosystem has at least one active partner present within that capability. Coverage reflects the presence and breadth of ecosystem partnerships; however, it does not measure quality, depth, or commercial success.

Developing an ecosystem takes time. It is an expensive and complex undertaking for a coretech vendor to manage the certification, onboarding, and support of new and existing partners. Progress often depends on partner availability and readiness. Even highly capable coretech vendors cannot quickly fill in their ecosystem maps. Gaps in coverage are normal, not necessarily a sign of weakness. Coverage (or lack thereof) is often intentional and provides an important signal about the coretech vendor’s strategic direction.

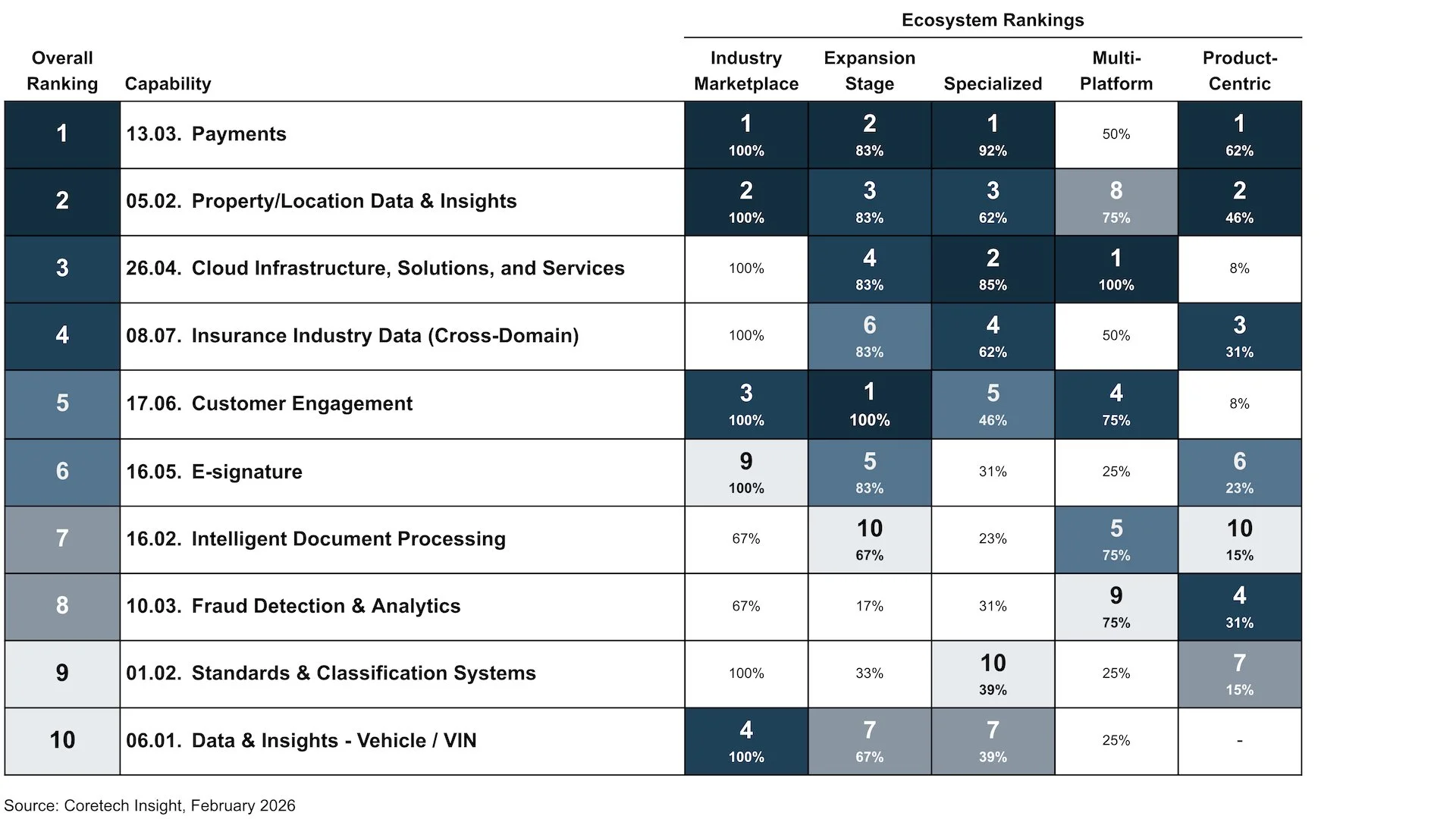

Top 10 Ecosystem Capabilities

Applying the 177 capabilities, every ecosystem provides a unique fingerprint. Across all ecosystems, there are also capabilities that many (sometimes nearly all) coretech vendors cover. These capabilities with near-universal coverage highlight industry norms and shared buyer expectations.

Figure 5 shows the top 10 capabilities ranked by coverage across all vendors, and within each of the 5 ecosystem types — Industry Marketplace, Expansion-Stage, Specialized, Multi-Platform, and Product-Centric. (For a detailed overview of ecosystem types, see Ecosystems as Strategic Signal: Five Types of Coretech Ecosystems.)

Figure 5. Top 10 Ecosystem Capabilities

These Top 10 capabilities are commonly found in mature coretech ecosystems. They reflect operational necessity and baseline expectations. They are not necessarily strategic or innovative, though, and capabilities not in the top 10 are not lower value. Many of the capabilities with less coverage reflect specialization and/or early adoption of emerging technologies.

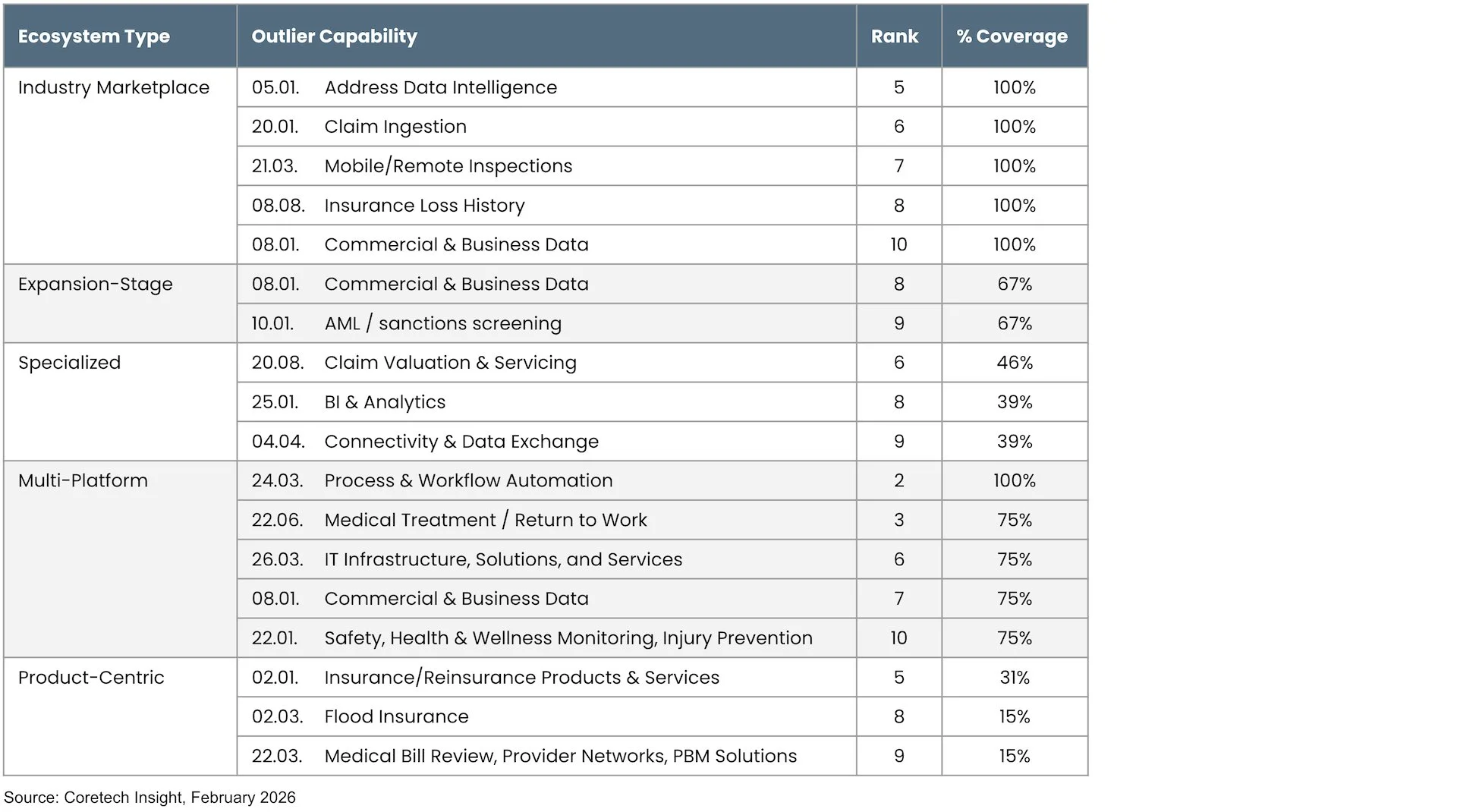

Reviewing each of the five ecosystem types, we find that some of the top 10 capabilities within each ecosystem were outliers that did not make the overall top 10 (see Table 1).

Table 1. Ecosystem Capability Outliers (Areas of Special Emphasis)

These outliers provide important clues about focus and adoption within the different ecosystem types. While the top 10 capabilities reveal areas of high maturity with lower differentiation, the outliers reflect unique emphasis and greater buyer demand within each type, and may indicate emerging norms or potential areas for future ecosystem expansion.

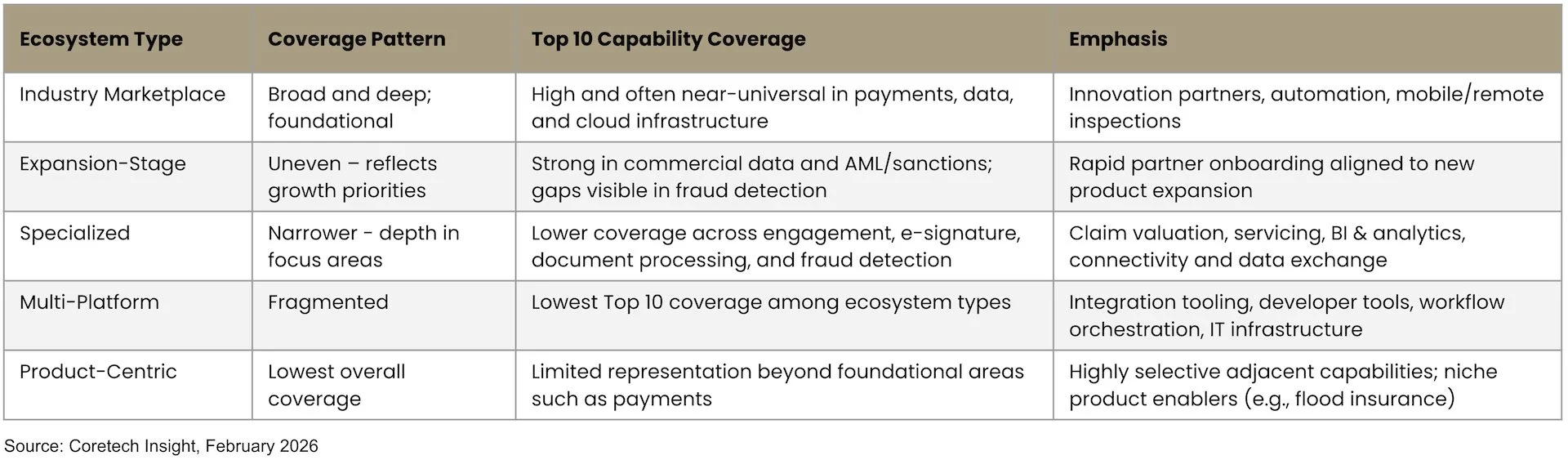

Table 2 below summarizes coverage patterns and special emphasis observed across each ecosystem type.

Table 2. Ecosystem Coverage Patterns and Special Emphasis

Key Signals from Ecosystem Coverage

Ecosystem coverage can be a useful measure of the health of a coretech vendor, as building and sustaining a successful ecosystem requires a certain level of maturity and capability. Technical maturity is needed for appropriate architecture and API capabilities, including tooling and documentation. Managing partner certification, onboarding, and support requires a sufficient level of operational discipline and resources. A coretech vendor must also have sufficient market credibility to attract third parties willing to partner and invest in a relationship.

Coverage also signals a vendor’s strategy. Broad coverage may reflect an ambition to operate at scale in a platform business model. Narrow coverage can indicate a focused strategy with specialization in specific segments. The key is whether a vendor’s messaging matches its ecosystem pattern. Narrower ecosystem coverage when a vendor promotes a specialized focus is more likely to be aligned and appropriate. Narrower coverage when a vendor’s messaging promotes expansive capabilities is a disconnect that may indicate gaps at both the ecosystem and underlying platform levels.

Evaluating Ecosystem Fit

A core platform that is a strong contender for a particular market segment should be accompanied by a robust cadre of appropriate ecosystem partners. Buyers understand they are selecting more than a platform; with their decision, they are buying into an operating model, partner network, and a pace of innovation.

Buyers should review the categories and capabilities, identify those essential for their business, and then look for matching ecosystem coverage. The expansive coverage of coretech vendors with Industry Marketplace Ecosystems gives them a general advantage. However, on a case-by-case basis, the coverage of other ecosystem types may be an equal or better fit.

For a Regional Carrier – Vendor A or Vendor B?

Imagine a $250M DWP regional insurance carrier supporting personal and commercial lines is seeking a new core platform. It wants to modernize and replace its legacy systems for policy, billing, and claims. The new platform should also support digital channels and provide data and analytics capabilities. The carrier is considering two platforms (real-world examples anonymized) and is applying the ecosystem mapping framework as part of its selection process.

Both ecosystems are the same size, and they both cover the following 13 capabilities:

Table 3 shows the remaining distinctive capabilities (relevant for this scenario) covered by each ecosystem.

Table 3. Coretech Ecosystem Coverage - Vendor A vs. Vendor B

Based on this mapping, Vendor A’s ecosystem shows strength in essential areas, such as standards and statistical reporting, property and VIN data, and claim servicing. Its coverage indicates an ecosystem that is carrier-focused, operationally grounded, aligned with traditional distribution, and prepared for regulatory and reporting requirements. Vendor B’s ecosystem is more workflow-driven, oriented toward digital experience and automation, and leans toward product experimentation. For a regional carrier that prioritizes operational stability, agency connectivity, and reporting, Vendor A’s ecosystem provides a better fit.

However, if we imagine a different scenario – for example, one of a carrier or MGA that needs to launch a new, digital-first product – the picture changes. Vendor B’s ecosystem offers advantages in workflow, automation (including emerging agentic systems), and data & analytics. Its ecosystem supports digital products, customer journey management, automated underwriting flows, and tooling for front-end engagement. For a carrier prioritizing digital UX, workflow configurability, and automation-driven growth, Vendor B’s ecosystem is a better fit.

The Path Forward

This assessment framework is a starting point. Too often, the primary measure of coretech ecosystems has defaulted to the number of partners. However, a large number of partners does not guarantee coverage aligned with buyer needs. This framework helps buyers orient, compare ecosystems, and ask better questions. It is not intended to rank vendors or prescribe the ideal ecosystem shape.

Coretech ecosystems have greatly increased in importance over the last decade, and especially over the last five years. For buyers, ecosystems offer a faster path to new capabilities and technologies. For vendors, ecosystems enable them to extend their reach, differentiate, and add new business models and revenue streams. Understanding ecosystem coverage helps buyers and vendors come together and align on implementations and innovation paths. This framework is intended to help provide a shared language for these essential conversations.

Recommendations

Coretech Buyers:

Identify the specific ecosystem capabilities that matter to you—to your LOBs, the size of your organization, your operating model, and workflows. Use these to evaluate coretech ecosystems and identify any gaps upfront so they can be managed, and not left to be discovered during implementation.

When evaluating coretech ecosystems, focus on whether coverage aligns with your current needs, and gaps align with your tolerance for custom integration. No ecosystem covers everything. Favor vendors that are transparent about where their ecosystems are strong and where they are thin.

Use the ecosystem capability framework to compare ecosystem shape, along with size. Two vendors with similar-sized ecosystems often have very different capabilities. Ask vendors to explain why their ecosystem looks the way it does, and how they expect it to evolve over time.

Incorporate ecosystem capabilities and roadmaps into your long-term planning. Look beyond immediate fit with short-term requirements and evaluate how well each ecosystem aligns with your strategic objectives and plans for future technology adoption.

Coretech Vendors:

Audit your ecosystem claims against the reality of your supported capabilities. Identify gaps that are defensible and those that are a strategic weakness. Align your messaging with reality to build credibility with buyers.

Position ecosystem gaps as signals, not shortcomings. Be explicit with buyers about where you choose to invest and where you do not based on your market focus. Buyers will understand strategic, intentional gaps, but question the unexplained.

Use the capability framework to prioritize ecosystem investment. Sequence your ecosystem expansion and recruit partners for capabilities where ideal customer demand is present or emerging, but ecosystem coverage is thin.

Encourage buyers to use a framework approach for evaluating ecosystems. Buyers are placing more emphasis on ecosystems and are increasingly sophisticated in their evaluation. Vendors who are transparent and help buyers interpret coverage will be perceived as more knowledgeable and better long-term partners.

Ecosystem Partners:

Use capability coverage to look beyond ecosystem size to identify opportunities. These capabilities show where ecosystems are crowded and where they are underserved. Look for capabilities with uneven coverage where buyer demand exists, but has not been served across all ecosystem types or market and submarket leaders.

Identify adjacent capabilities that may flag potential opportunities. Look for coretech vendors building out capabilities that complement or are precursors to your offerings. You may be a natural and desirable fit for the direction their ecosystem is evolving.

Match your partner strategy to the appropriate ecosystem type and shape. Go where your customers are and where ecosystem maturity supports adoption. Avoid spreading resources across poorly aligned or incompatible ecosystems.

Periodically revisit and revise your assumptions about the market. Use this framework to assess which categories are becoming commonplace, and which remain or are emerging as differentiators, and incorporate these updates into your planning and product roadmaps.

For organizations seeking to apply this capability framework — including detailed ecosystem benchmarks, vendor-specific insights and comparisons, and strategic fit assessments — Coretech Insight provides private research reports and executive briefings tailored to buyers, vendors, and ecosystem partners.

To explore a private briefing or customized research engagement, contact Coretech Insight at jeff.haner@coretechinsight.com.

Note 1. Methodology

This article builds on ecosystem research conducted by Coretech Insight in Q4 2025. The research analyzed publicly available ecosystem, partner, and marketplace content for 39 P&C coretech vendors actively marketing in the United States and Canada.

We reviewed ecosystem presentations, partner directories, marketplace listings, and more than 450 press releases announcing technology partnerships over the past 15 years. From this analysis, we catalogued 647 ecosystem partners and developed a structured capability framework comprising 30 first-level categories and 177 second-level capabilities.

Each capability was assessed for coverage based on the presence of at least one publicly announced partner within that capability area. This research is designed to identify structural ecosystem patterns and strategic emphasis — not to audit integration depth, contractual status, production usage, or commercial success.

Important caveats:

This analysis focuses on technology and solution partners. Ecosystem partners were included when they provide integrated technology solutions, applications, or platform extensions typically reflected in partner directories or marketplaces. Professional services firms, system integrators, and implementation partners were not included, as this research evaluates ecosystem capability coverage rather than delivery capacity.

Partnership inclusion reflects vendor-acknowledged relationships. This analysis includes ecosystem partners publicly identified by coretech vendors in press releases, partner directories, or marketplace listings. Some technology providers may independently claim partnerships that are not formally announced by the coretech vendor. Such claims were not included in order to maintain consistent inclusion criteria across vendors.

Public information may be incomplete. Some vendors maintain integration libraries or partner relationships that are not fully disclosed in public materials.

Coverage indicates presence, not quality. A capability is considered “covered” if at least one partner exists in that area. This does not measure integration depth, deployment frequency, revenue contribution, or the maturity of the relationship.

Gaps may be intentional. Missing capabilities often reflect strategic positioning rather than technical limitations. Vendors prioritize ecosystem investment based on target markets, product strategy, and operating model.

This research represents a point-in-time analysis. Ecosystems evolve continuously, with new partnerships announced regularly. While Coretech Insight intends to update and refine this dataset periodically, this analysis reflects publicly available information as of Q4 2025.

Despite these limitations, publicly shared ecosystem content provides a meaningful signal of vendor strategy, partner prioritization, investment in extensibility, and the role ecosystems play in go-to-market execution. This approach enables consistent cross-vendor comparison using a common structural lens.

Jeff Haner is the co-founder of Coretech Insight, an independent advisory firm. He has served in senior IT, advisory, and marketing roles with Deloitte, Oliver Wyman, NJM Insurance Group, Gartner, and BriteCore. While with Gartner, he authored the Magic Quadrant for P&C Core Platforms. Jeff’s experience “on both sides” of the insurance technology table and his ongoing research enable him to offer deep insurance industry knowledge, strategic insights, and hands-on help to take action.

Contact Jeff at jeff.haner@coretechinsight.com