Early Indicators 2025 Recap: Ecosystems and AI are Transforming the Coretech Market

This is an update to Coretech Insight’s ongoing review of publicly announced coretech deals with P&C insurers.

Repeating a pattern set in 2024, announced coretech platform and system deals in 2025 fell to historic lows.

The coretech market has changed. Market leaders have shifted their focus from “landing and expanding” to “farming” with cloud platforms and ecosystems, enabled and accelerated by AI and other emerging technologies.

Leaders are thriving in this new market; others are scrambling to adapt.

We anticipate a scenario where 30-40% of current vendors will be acquired or exit by 2030.

Analysis

New Selection Announcements At Historic Lows

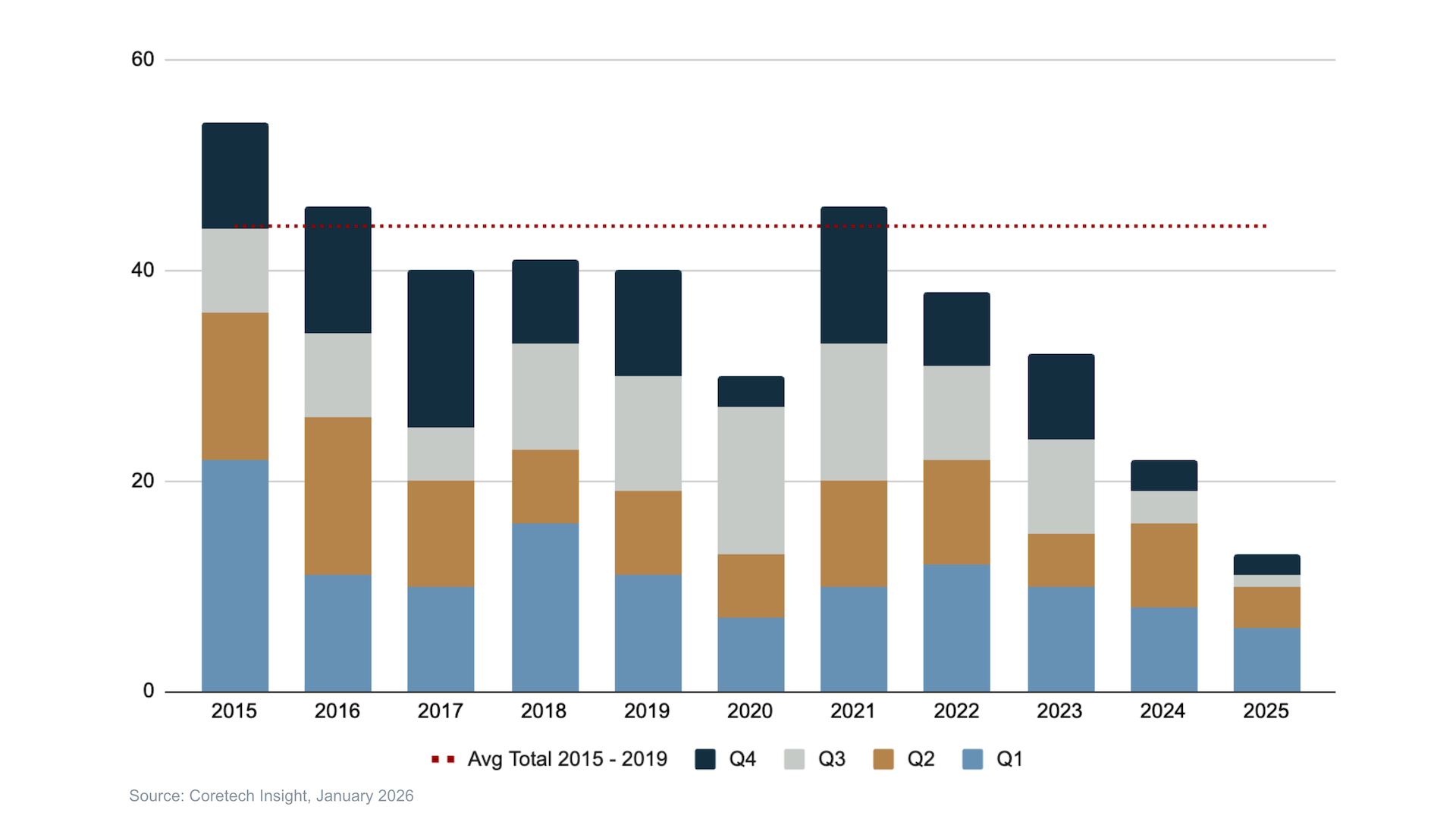

In Coretech Insight’s review of P&C core platform deal announcements, 2025 set a new low, with 40% fewer new deal announcements in 2025 than in 2024 (see Figure 1).

Figure 1. Announced P&C Coretech Selections by Quarter, 2015 - 2025

Note: These totals do not reflect all new system selections. We estimate these cover 30 to 40% of all selections from P&C insurance carriers, MGAs/MGUs, and other entities such as risk pools and TPAs. Although not a complete record of all public and private deals, these announcements are valuable as a publicly verifiable record. See Note 1. Methodology below for more details.

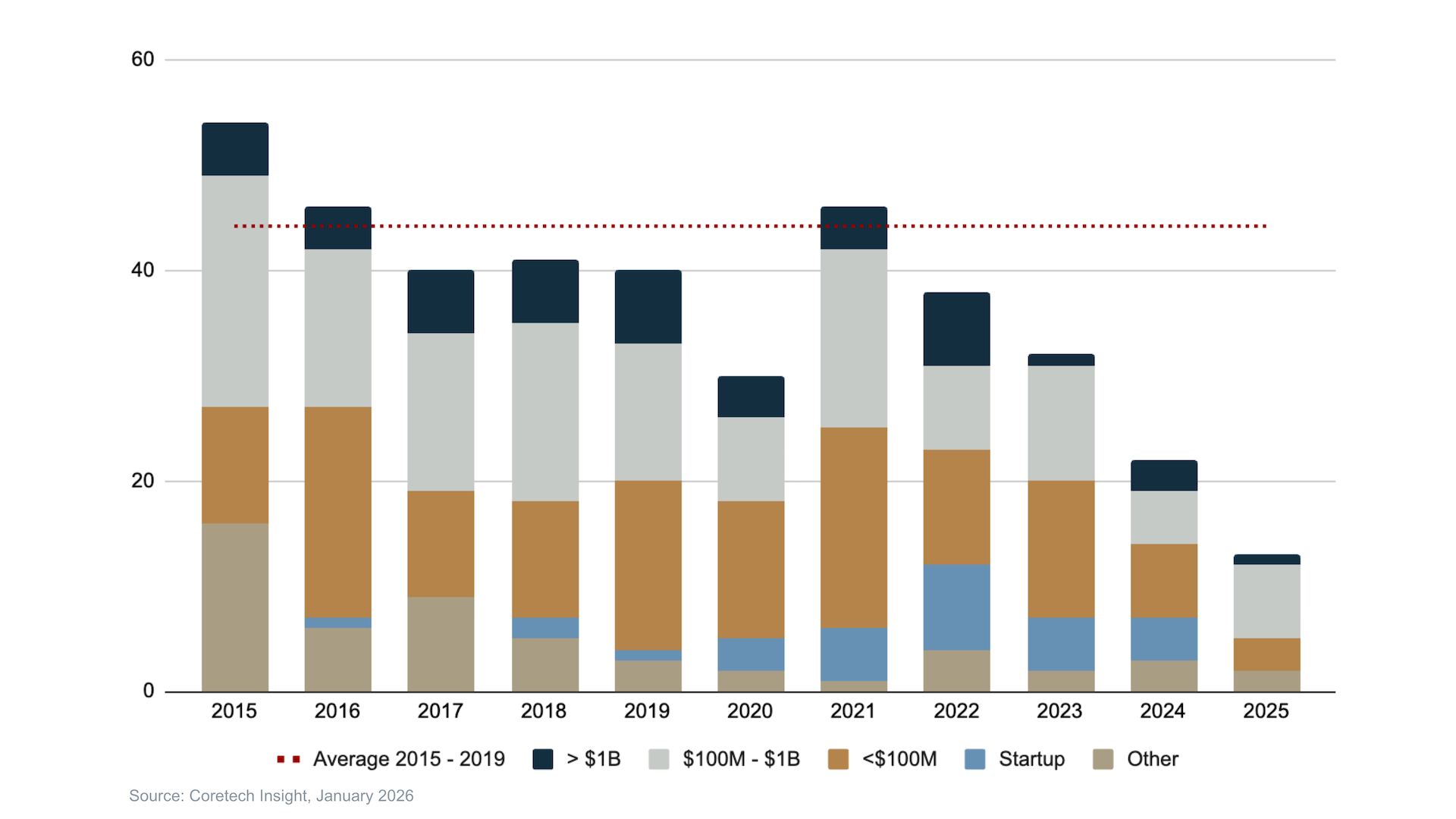

This decline occurred among insurers of all sizes and premium tiers except SMB insurers, those with DWP between $100M and $1B. In contrast to other premium tiers, announced deals with SMB insurers increased slightly from five in 2024 to seven in 2025. (See Figure 2.)

Figure 2. Announced P&C Coretech Selections by Premium Tier, 2015 – 2025

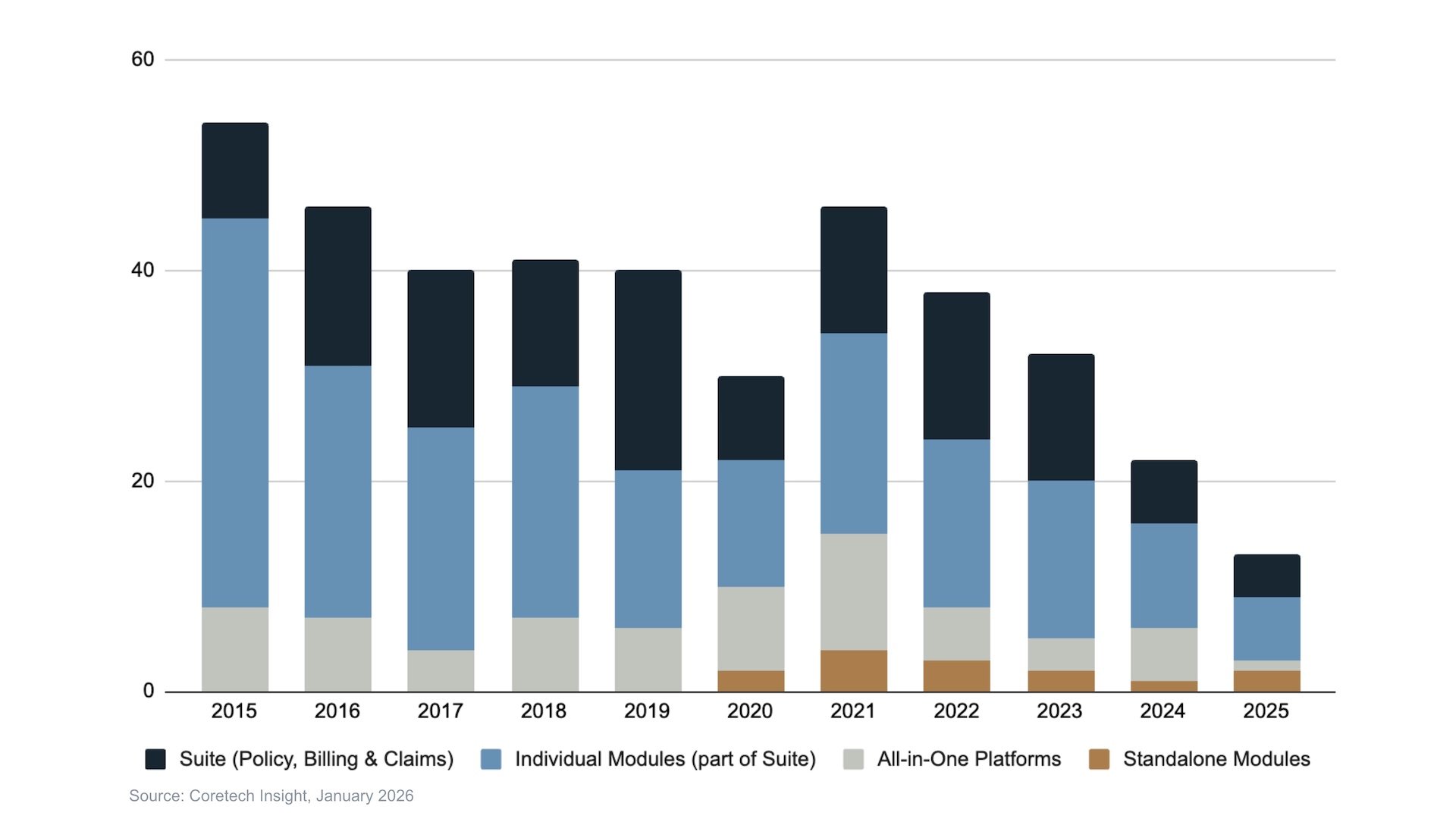

Nearly all selection announcements were for modular platforms featuring full suites with integrated core modules, or for individual policy, billing, or claims modules within a broader suite. (See Figure 3.)

Figure 3. Announced P&C Coretech Selections by Solution Type, 2015 - 2025

This emphasis on core suites and integrated modules continued a shift toward established platforms for legacy modernization that followed the post-pandemic peak of announcements in 2021. Nearly all of the top five vendors (for number of announced selections) from 2022 through 2025 offer modular platforms with full core suites, and serve large and well-established customer bases:

Guidewire

Origami Risk

Cogitate and Socotra (tied for third place)

Five Sigma

Duck Creek, Majesco, and Sapiens (tied for fifth place)

A Fundamentally Different Market

In our prior market recap articles, we’ve spotlighted individual external factors, such as the disruption of the pandemic, challenging economic conditions, and uncertain political/federal government policy, that have raised the level of risk for buyers and reduced their appetite for new systems.

Taking a step back and reviewing the last six years, P&C insurance business and technology leaders have had to navigate a series of significant challenges:

2020 - A pandemic shuts the world down. New projects are suspended as focus shifts to weathering lockdowns and pivoting to digital-first operations.

2021 - The world reopens. Pent-up demand plus a large inflow of investment capital into insurtechs drives a near-record year for coretech system selections.

2022 - Significant underwriting losses dampen appetite for large IT initiatives.

2023 - Ongoing underwriting losses and unprecedented P&C insurance industry layoffs depress demand.

2024 - Mild recovery for the insurance industry, but an acrimonious US presidential election between parties with starkly different visions drives uncertainty and caution. Coretech system selection announcements decline to a historic low.

2025 - Economic and market volatility, tariff uncertainty, and uncertainty over AI adoption prompt buyers to remain cautious. The US economy as a whole sees the largest layoffs since 2020. For the second year in a row, coretech system selection announcements decline to a new historic low.

Layered over this backdrop of external challenges has been growing fatigue and disappointment with ambitious, large-scale core platform replacement projects. As often happens with enterprise software implementation, many core platform initiatives have been over time, over budget, and have delivered less value than anticipated. There have been several high-profile failures and many unpublicized disappointments.

The picture that has emerged is not one of a market about to recover from a few temporary setbacks. The trajectory of the market for P&C core systems has been fundamentally altered. Cautious insurance leaders have little appetite for large-scale, high-risk core system initiatives with uncertain ROI. Buyers demanding short paths to business value have driven smaller deal sizes with faster payback, often building on or extending existing systems rather than adopting new ones. The rapid emergence of AI has opened new possibilities for reusing and extending current technology assets. Gone (for now) are the pre-pandemic days of 100+ new core system selections each year, with many bold and expansive rip-and-replace initiatives.

The Ecosystem is the Platform

This fundamental shift has accelerated a shift in focus from suites and platforms toward ecosystem-driven business models – an evolution that was already beginning in the mid to late twenty-teens. The growing number of third-party integrations and partners forming around ascendant core platforms was first promoted to buyers as a competitive differentiator. Partner numbers grew, programs were formalized, and these collections began to morph into ecosystem marketplaces.

Today, a strong core platform plus a robust ecosystem offers buyers a fast track to new capabilities and business value. Rather than assembling and maintaining a mix of core systems and custom integrations, buyers can select a platform with comprehensive core capabilities and pre-integrated access to third parties. The modular nature of most platforms enables buyers to adopt new core modules and components in manageable stages, while offering the flexibility to mix and match ecosystem partners within the safe confines of a curated marketplace.

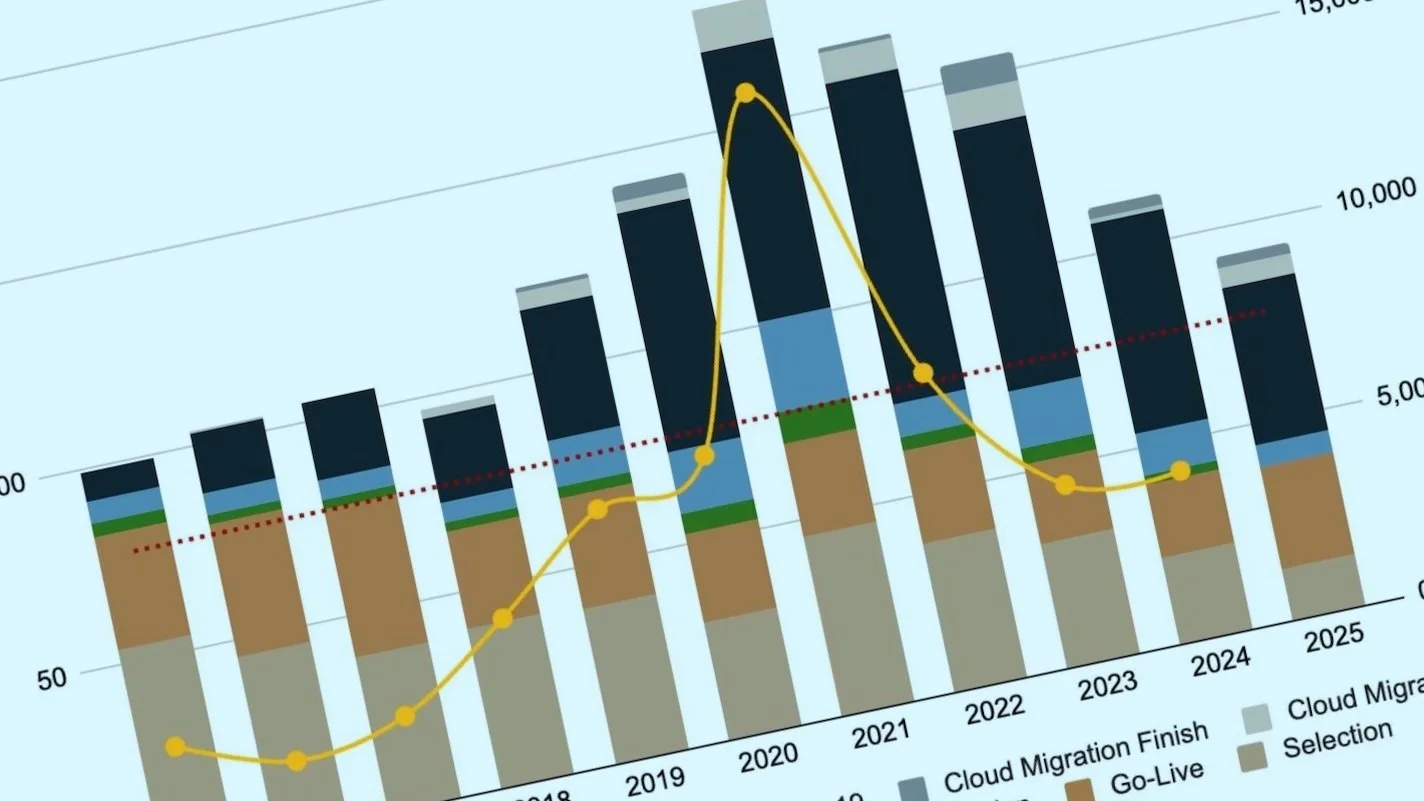

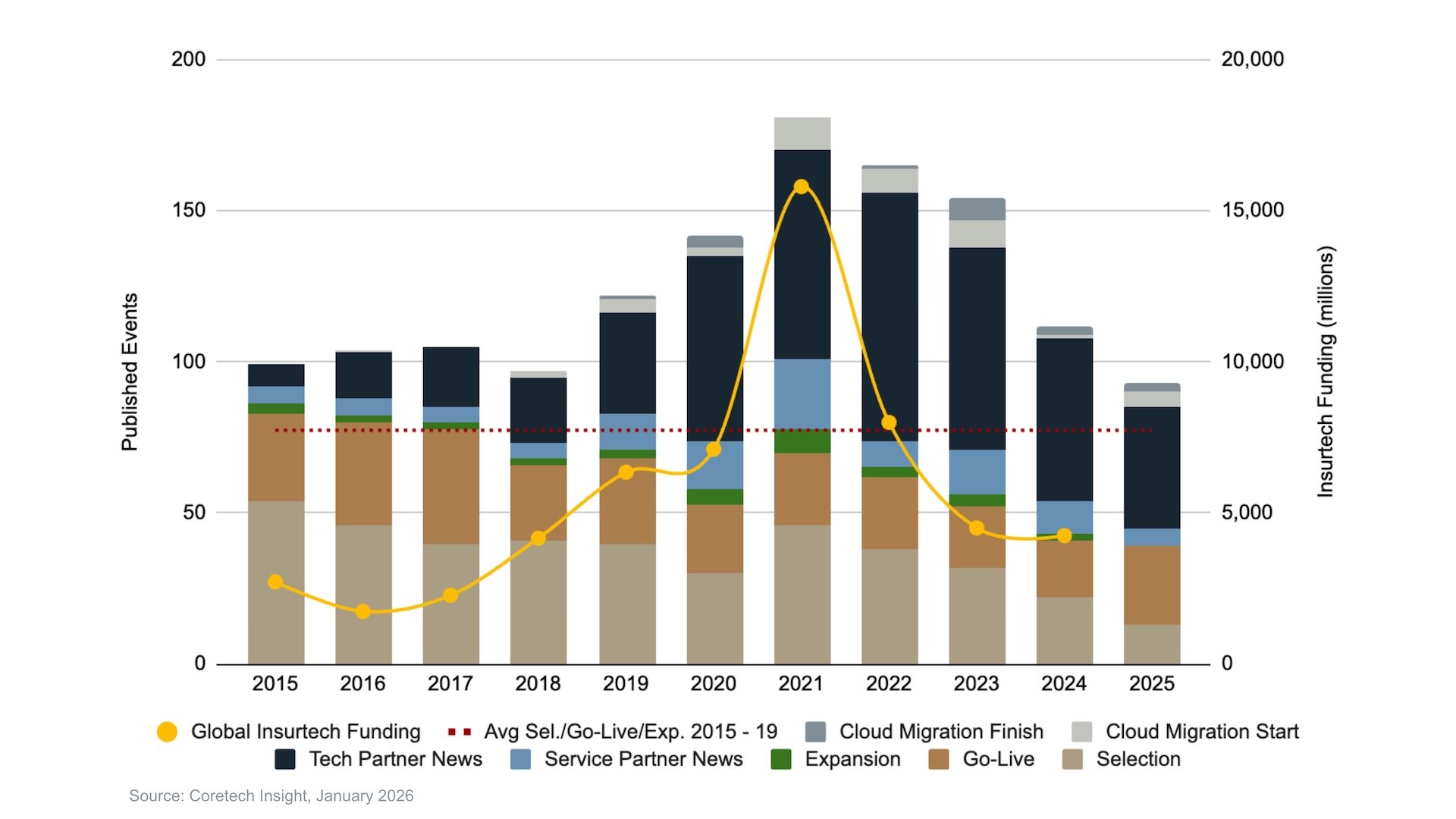

As new system deals declined, and coretech vendors began to hunt for new revenue streams, partner ecosystems (along with cloud migrations) stepped into the gap. We see this reflected in the surge in press releases on ecosystem partners and cloud migrations over the past six years, as shown in Figure 4. Looking at how things started compared to how things ended over this period, ecosystem partner and cloud migration announcements were only 13% of press releases in 2015; this percentage had risen to 58% by 2025.

Figure 4. P&C Coretech Announcements - Selections, Go-Lives, Expansions, Partners, and Cloud, 2015 - 2025

Note: Global Insurtech Funding per Gallagher Re: Global InsurTech Report for Q3 2025

A skeptical observer might conclude these announcements are meaningless — ecosystem theater by coretech vendors promoting partnerships in an attempt to preserve a growth narrative. In some cases, this may be true. It takes little effort to reach an agreement with a third-party, issue a press release, and add a logo to a website, which might help convey a sense of continued momentum in the absence of new customer deals to share.

Installed Base is the New Growth Engine

However, as coretech vendors have shifted their focus to expanded monetization of existing customers and partners, those with robust ecosystems – true integrations and partnerships that extend functionality and deliver business value – have a great advantage.

The ecosystem becomes more than a nice-to-have differentiator; if it delivers real business value, it can increasingly function as a toll road on which coretech vendors can charge partners and customers alike for access and ongoing use. Each new partner announcement represents new upfront revenue and an ongoing revenue stream, potentially multiplied over hundreds of customers.

Cloud migrations – common but less prolific than ecosystem announcements – also provide vendors with a significant source of revenue. Cloud migrations require professional services and often take more than a year to complete. Afterward, the ongoing SaaS subscription fees are typically double or triple (or more) the licensing fees of formerly on-prem deployments.

The move to the cloud over the last decade and a half has also given coretech vendors – with or without ecosystems – another simple, powerful lever for securing additional revenue: price increases. With SaaS subscriptions, customers have less independence than with on-prem deployments with traditional software licensing. At renewal or annually (depending on the subscription), a coretech vendor can make it a routine practice to announce subscription price increases. In the short-term, at least, customers have little choice but to continue paying for access.

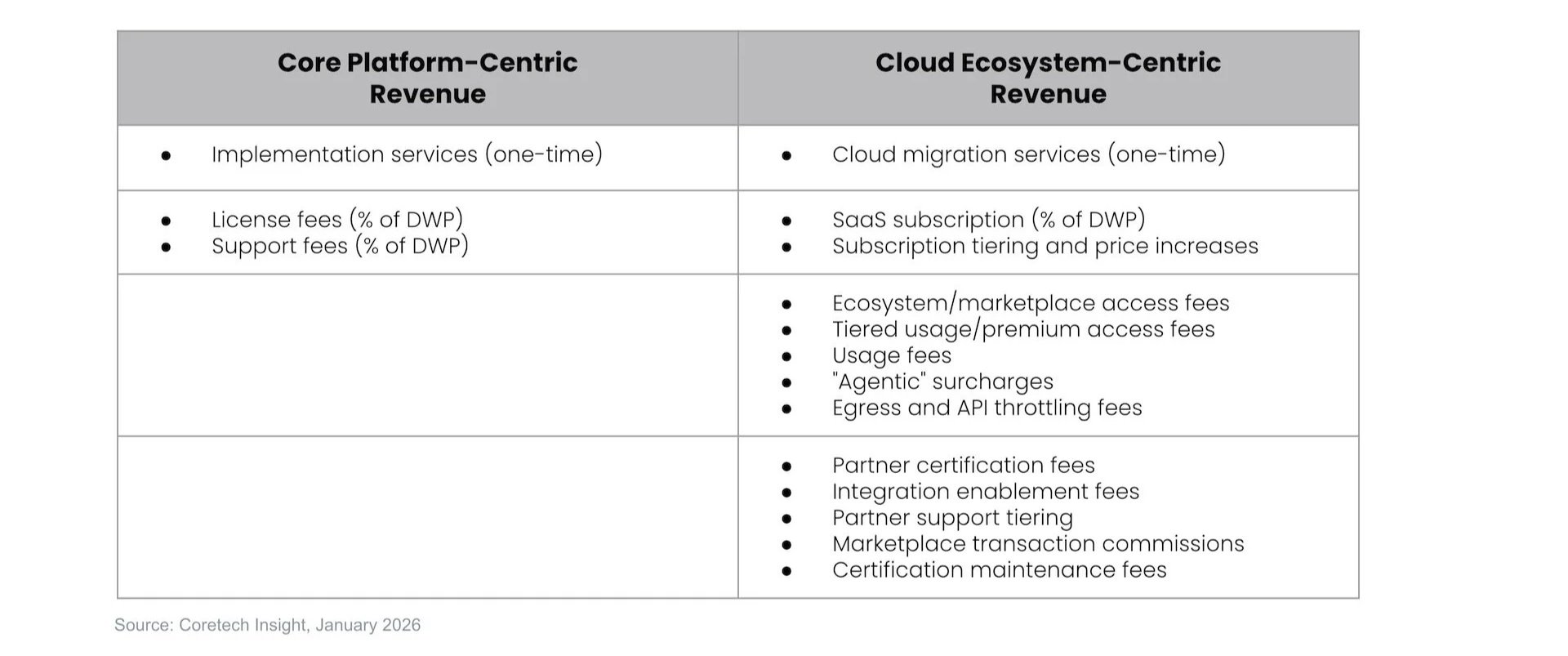

As Table 1 shows, the move from a traditional core-centric model to a cloud-based ecosystem model opens up a variety of new, ongoing revenue streams, such as cloud migration services, ecosystem enablement fees, access fees, and tiering surcharges. The cumulative impact of these new revenue streams can be substantial. This shift has enabled well-positioned vendors to weather external challenges and thrive over the last few years, even as the number of new system selection announcements has declined.

Table 1. Core Platform (On-Prem) vs. Cloud Ecosystem Revenue

More Consolidation on the Way

There are, depending on how the lines are drawn, about 50 P&C core system/platform vendors actively marketing their solutions in the US and Canada. Many of these vendors are poorly positioned for this new market, which prioritizes ecosystem breadth and depth, and in which expansive system selection deals are less common.

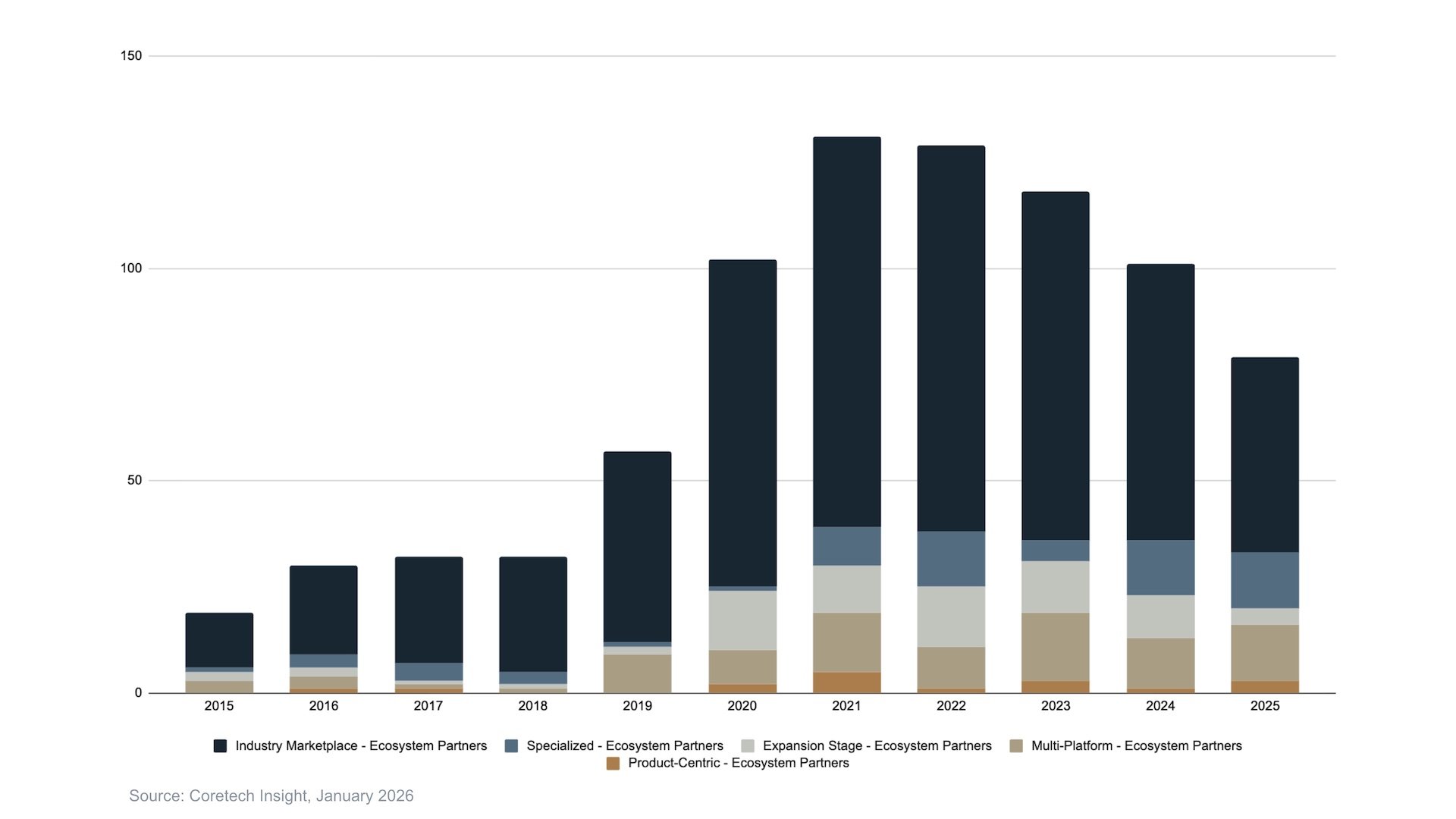

In Coretech Insight’s article Ecosystems as Strategic Signal: Five Types of Coretech Ecosystems, we reviewed 39 coretech vendors with over 600 ecosystem partners, and identified five types of coretech ecosystems that have emerged over the last decade. As Figure 5 shows, the vast majority of ecosystem announcements have come from a subset of vendors that have built broad industry marketplaces, followed by others that are proactively focused on ecosystem expansion or specialized ecosystems.

Figure 5. P&C Coretech Partner Announcements by Ecosystem Type

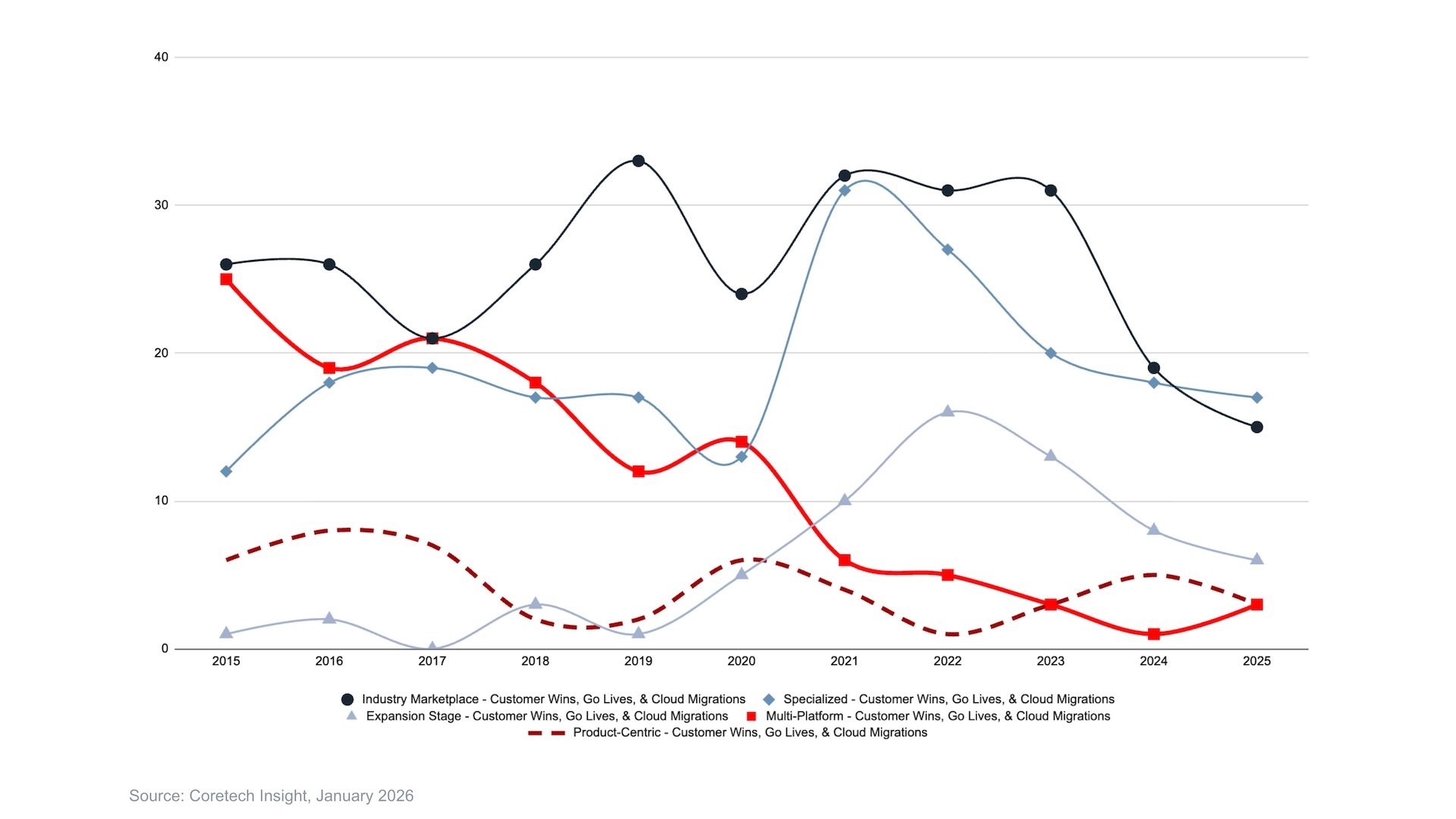

As Figure 6 shows, vendors with Industry Marketplace Ecosystems, Expansion-Stage Ecosystems, or Specialized Ecosystems (56% of those reviewed by Coretech Insight) have had greater customer activity, including announcements for new selections, go-lives, expansions, and cloud migrations. In contrast, vendors with a more reactive posture, with product-centric or fragmented, multi-platform ecosystems (44%), have reported low or declining customer activity. While ecosystem maturity is no guarantee of commercial success, it is correlated with observable customer activity in this market.

Figure 6. P&C Coretech Wins, Go-Lives, and Cloud Migration Announcements by Ecosystem Type

In prior articles (see Early Indicators 2024 Q1 — Public Coretech Deals Set New Quarterly Low), we’ve catalogued a number of mergers and acquisitions that have already taken place over the last few years. This M&A activity will accelerate, as fundamental changes in the market have rendered the business models of many vendors obsolete. Coretech Insight expects a scenario where 30-40% of current vendors are acquired or exit the market by 2030. The pace and form of consolidation, though, will vary depending on vendor circumstances, from outright acquisitions to slower wind-downs. Some coretech vendors will reinvent themselves, piggyback on other established ecosystems, and become a partner with specialized, core-adjacent capabilities.

AI is Accelerating Market Change

AI adoption is accelerating these trends and widening the gap between market leaders with robust, operational ecosystems and those with less mature marketing ecosystems. Market leaders are using ecosystems to attract and rapidly integrate AI-enabled partners with new and innovative capabilities. These leaders are embedding AI into their core platform offerings to deliver more intelligent core processing. Behind the scenes, they’re also incorporating AI-enabled development tools and practices to accelerate their product roadmaps.

Advances in AI-enabled development are also changing the build-vs-buy calculation for insurers. A key argument for buying instead of building has been the sheer effort required – hundreds of IT resources – to build and maintain an enterprise-class P&C core platform. AI-enabled development has significantly compressed the time and resources required for analysis and documentation, routine coding, testing, and coordination. Based on early adopter experience, this translates into teams that can be 30% to as much as 50% more productive in software delivery and maintenance workflows. The cost to develop software is dropping significantly.

AI-enabled development is expanding the number of scenarios where in-house development, once unthinkable, may be a viable option. This is especially true for more sophisticated, tech-forward insurers with existing software engineering capability, a narrower market focus, those who prize data sovereignty, and those with nonstandard workflows or proprietary methodologies outside industry norms. For these insurers, AI-enabled in-house development may provide solutions with a better fit and value than commercial SaaS coretech solutions, along with lower, more easily controlled long-term costs.

The net effect of these changes will be increased pressure on vendors that have not yet successfully transitioned to a cloud ecosystem model. There will be even fewer traditional selection deals available as market leaders expand the scope and value of their core platforms and ecosystems, and a growing number (although still a minority) of insurers begin to turn from commercial solutions to AI-enabled alternatives.

Looking Ahead

Looking to 2026 and beyond to 2030, Coretech Insight expects to see:

Continued dominance of market leaders with expanding ecosystems

Increasing consolidation among declining vendors with limited ecosystem capabilities

Growing buyer frustration with rising costs and expanding matrices of fees

A resurgence of in-house build initiatives fueled by AI-enabled development

The next few years will be very interesting.

Recommendations

Coretech Buyers:

Use ecosystem type as a strategic signal of vendor health and trajectory. Those with Industry Marketplace or Expansion-Stage Ecosystems demonstrate stronger positioning. (See Ecosystems as Strategic Signal: Five Types of Coretech Ecosystems.) Evaluate ecosystem maturity, governance, and economics with the same rigor applied to core system and platform selection, and select vendors with robust, active marketplaces.

Model long-term total cost of ownership (TCO) across the entire ecosystem, not just the core. Expect a range of new and different fees – subscription, access, integration, usage, and premium tiering – that may hit different parts of your organization and be difficult to identify and monitor. Five to ten-year TCO scenarios are essential.

Negotiate price protection. Some of our long-term models show a potential for cumulative 200%+ increases over a 10-year horizon if left unchecked. Push for price caps, feature preservation, and platform support commitments.

Monitor vendor health and prepare exit strategies. Watch for red flags like stagnant innovation or financial distress. Negotiate contracts with strong SLAs, source code escrow, and transition support. Contractually ensure you can extract bulk data without punitive egress fees or throttling.

Coretech Vendors:

Conduct an honest assessment and take action. The market no longer supports dozens of undifferentiated platforms. If your core or ecosystem is lacking, narrow your focus, partner up, or proactively prepare for consolidation.

Build operational ecosystems that deliver value. Buyers will distinguish between low-value marketing ecosystems and high-value operational ecosystems. Customer adoption, repeat integrations, and coretech vendor and ecosystem partner collaboration matter more than claims about ecosystem size.

Ensure a favorable balance between new fees and new business value. Resist the urge to purely extract revenue through fees. Instead, co-innovate with your base. If your fees outweigh business value, your customers will build around you.

Ecosystem Partners:

Choose ecosystems deliberately and invest deeply, not broadly. The economics favor dominance in a few strong ecosystems, with only a moderate or opportunistic presence in others. Go to the ecosystems where your customers are. Partner ROI depends on ecosystem maturity and repeatability, not total logo count.

Budget for ecosystem monetization on the part of coretech vendors. Certification fees, revenue share, integration maintenance, and premium placement are likely to increase as ecosystems become revenue levers for core platform vendors.

Treat the ecosystem as a distribution channel, not a savior. Do not assume a partnership with a market-leading ecosystem will solve all your sales challenges. Weigh ecosystem results and “tolls” (such as revenue share, integration maintenance, and usage fees) against the success and cost of direct sales, and invest in each accordingly.

Monitor coretech vendor health, and protect IP and data. Do not bet your future on a single ecosystem. 30% to 40% of current coretech vendors are likely to be acquired or exit the market by 2030. Negotiate robust NDAs and non-exclusive terms to safeguard proprietary tech amid shared collaborations.

For readers seeking a deeper view of buying trends and the state of coretech ecosystems — including comparative assessments, partner category coverage, and vendor and core platform-specific insights — Coretech Insight offers private research reports and executive briefings. These are tailored to buyers, vendors, and ecosystem partners.

Readers interested in private reports or executive briefings are invited to contact Coretech Insight at jeff.haner@coretechinsight.com.

Note 1. Methodology

This research is part of Coretech Insight’s ongoing review of press releases (PRs) from P&C core platform vendors announcing the selection of their core platform or at least one core module (policy, billing, or claims) by US or Canadian customers. For this update, we broadened the scope of our review to include announcements for go-lives, expanded use, and the start and finish of on-prem to cloud migrations. We also included coretech announcements from vendors offering standalone modules (such as a claims management module) without a corresponding suite or platform.

The PRs reviewed for this research were published from 1/1/2015 through 12/31/2025 and featured on vendor websites and/or reported on by various wire services and news sites such as Business Wire, GlobeNewswire, PR Newswire, Insurance Innovation Reporter, and PropertyCasualty360.

Our objective with this review was to track buying activity and trends among insurance carriers and MGAs/MGUs. From the initial set of PRs we excluded:

PRs with no information on the timing of the events

PRs on customers that are not P&C insurance carriers, MGAs/MGUs, or other related P&C insurance entities

PRs on customers that are insolvent or no longer active

This review did not evaluate implementation timeframes or success rates — its focus was on the number and characteristics of selection decisions, go-lives, expansions, partnerships, and cloud migrations announced via press releases to gauge market activity and buying trends.

These public announcements do not reflect all new system selections or other vendor activities during this time period. For various reasons, such as client confidentiality, a conservative approach to promotion, or even a lack of marketing resources, vendors often do not publicize new wins, deployments, or other client activities. We estimate these press releases cover 30% to 40% of all new P&C core platform selections, go-lives, and expansions with P&C insurance carriers, MGAs/MGUs, and other P&C entities during these years.

Although not a complete record of all deals, these announcements are valuable because they provide a public, verifiable record with details jointly approved by buyers and sellers. They represent a high-quality and consistent sample of activity in the P&C core platform market.

Jeff Haner is the co-founder of Coretech Insight, an independent advisory firm. He has served in senior IT, advisory, and marketing roles with Deloitte, Oliver Wyman, NJM Insurance Group, Gartner, and BriteCore. While with Gartner, he authored the Magic Quadrant for P&C Core Platforms. Jeff’s experience “on both sides” of the insurance technology table and his ongoing research enable him to offer deep insurance industry knowledge, strategic insights, and hands-on help to take action.

Contact Jeff at jeff.haner@coretechinsight.com